Choosing Right People In Your Business

Picking a winning team in business requires a combination of art and science. Selecting a team with diverse skill sets and experiences and individuals who can work well together and communicate effectively is vital.

Choosing individuals that are great in their roles will only take you so far.

Attributes you should consider when looking at hiring are:

If you’re keen to explore changing accountants, we have a non-obligation process to do that. The first step is booking a strategy call with one of our accounting team. It’s a free 20-minute zoom or phone call where you get to meet us to manage your questions.

From that point, you can consider doing a “Look Under The Hood” with us. There is no obligation to change accountants, but we give you a second opinion if you’re paying too much tax.

Throughout that process, we can identify any problems we see with your current setup. Anything that your current accountant hasn’t claimed, or tax you may have overpaid, and strategies of how we might fix that going forward. We can run through with you once you book with us.

In a few years, employers may be required to pay super at the same time as wages

The Federal Government has announced that it’s considering amending super laws to require super to be paid on payday. The change is set to take effect from 1 July 2026, and it will aim to stop disreputable employers from exploiting their employees and avoid liability building up on the books.

This change may affect your cash flow if you are paying super quarterly. We suggest a staggered approach to pay employees super in the next two years. Start by increasing the frequency of paying super from three months to two. Do this for six months, then increase frequency to one month until your pay cycle aligns with super payment.

If you’re keen to explore changing accountants, we have a non-obligation process to do that. The first step is booking a strategy call with one of our accounting team. It’s a free 20-minute zoom or phone call where you get to meet us to manage your questions.

From that point, you can consider doing a “Look Under The Hood” with us. There is no obligation to change accountants, but we give you a second opinion if you’re paying too much tax.

Throughout that process, we can identify any problems we see with your current setup. Anything that your current accountant hasn’t claimed, or tax you may have overpaid, and strategies of how we might fix that going forward. We can run through with you once you book with us.

Do You Have a HECS-HELP Loan?

The Australian Government indexes HECS-HELP loans each year on the 1st of June.

The Australian Government indexes HECS-HELP loans each year on the 1st of June. The percentage in which the debt amount will go up is directly linked to the cost of living (i.e. inflation).

On the 1st of June 2023, the HECS-HELP loans are predicted to increase by up to 7-8%. If you have a HECS-HELP loan, consider making an early payment before 1 June 2023 if cash flow permits. Individuals with low balances might be tempted to clear their HECS-LOAN balance altogether.

If you’re keen to explore changing accountants, we have a non-obligation process to do that. The first step is booking a strategy call with one of our accounting team. It’s a free 20-minute zoom or phone call where you get to meet us to manage your questions.

From that point, you can consider doing a “Look Under The Hood” with us. There is no obligation to change accountants, but we give you a second opinion if you’re paying too much tax.

Throughout that process, we can identify any problems we see with your current setup. Anything that your current accountant hasn’t claimed, or tax you may have overpaid, and strategies of how we might fix that going forward. We can run through with you once you book with us.

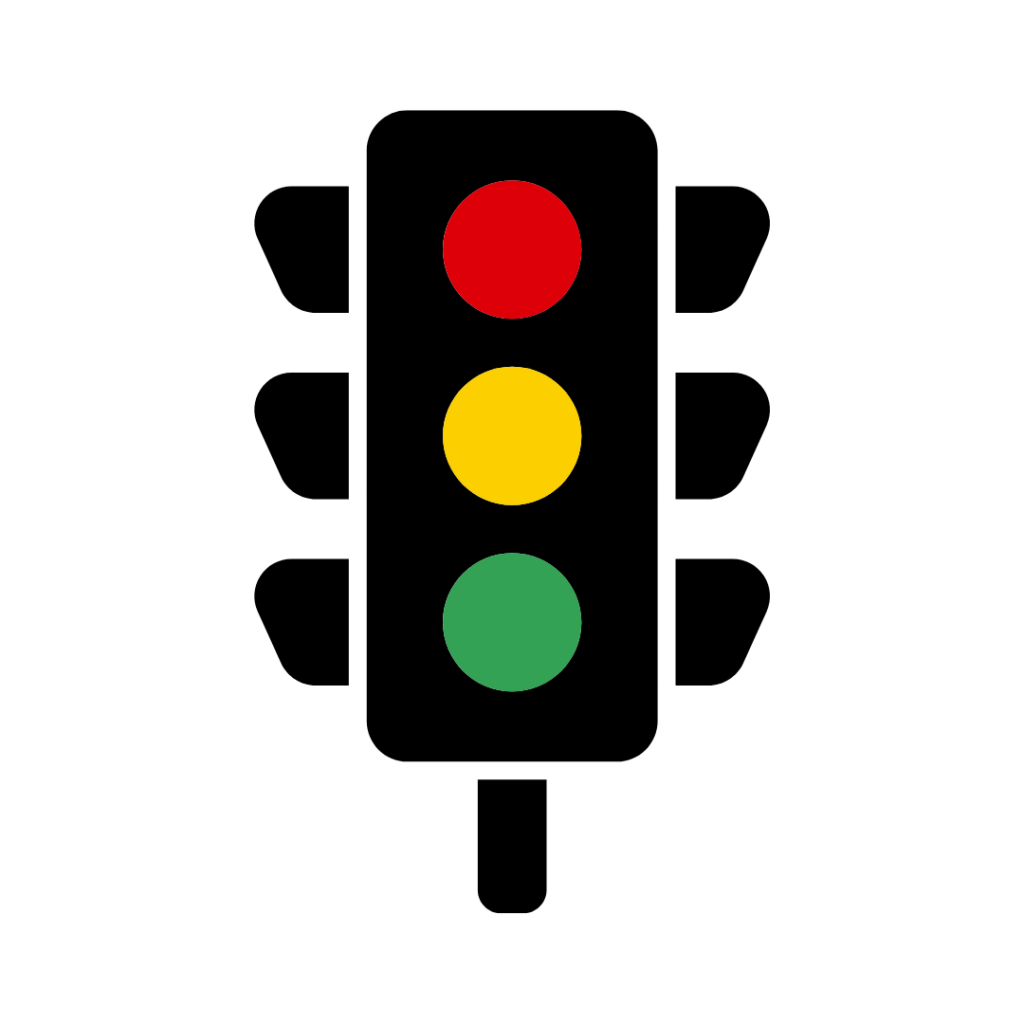

The Final ATO Ruling Affecting Trust Distributions

The ATO has finalised the section 100A ruling, which provides guidelines and a compliance approach to trust distributions. In essence, the ATO is concerned that the adult beneficiary who’s been made entitled to a trust distribution does not enjoy the economic benefit. More importantly, section 100A also focuses on taxpayers that enter into an arrangement that is not considered ordinary family or commercial dealing but merely a scheme to seek a tax benefit.

The ATO’s compliance approach uses three colour zones to determine whether the arrangement is Low or High risk. There are White (Low), Green (Low) and Red (High) zones.

The ATO made many available examples of what arrangements would be considered low or high risk.

We will discuss how section 100A will impact our clients during tax planning and whether their existing arrangements are in the White, Green, or Red zone.

If you’re keen to explore changing accountants, we have a non-obligation process to do that. The first step is booking a strategy call with one of our accounting team. It’s a free 20-minute zoom or phone call where you get to meet us to manage your questions.

From that point, you can consider doing a “Look Under The Hood” with us. There is no obligation to change accountants, but we give you a second opinion if you’re paying too much tax.

Throughout that process, we can identify any problems we see with your current setup. Anything that your current accountant hasn’t claimed, or tax you may have overpaid, and strategies of how we might fix that going forward. We can run through with you once you book with us.

How To Cut Energy Waste And Save Money

Small Business Energy Incentive is not too dissimilar to the small business skills boosts and investment boosts that we saw last year introduced by the previous government.

Basically, it’s allowing you an extra 20% tax deduction for any expenses that are related to the use of the word “electrification” and more efficient use of energy.

They are trying to make sure that any appliances that you have are a bit more efficient. The things like heating and cooling systems. And if you upgrade it to more efficient fridges, induction cooktops, installing batteries and heat pumps. Anything that makes the use of energy a bit more efficient, will be eligible for what we call a 20% extra deduction.

There is a limit of up to a hundred thousand in total expenditure. The way that this was announced was for restaurants, hair dresses, or we’ve got anything that had used the premises. If you have things that are using electricity right now and you can make it a bit more efficient, this is where you’ll be able to get an extra $20,000 extra deduction there.

If you’re keen to explore changing accountants, we have a non-obligation process to do that. The first step is booking a strategy call with one of our accounting team. It’s a free 20-minute zoom or phone call where you get to meet us to manage your questions.

From that point, you can consider doing a “Look Under The Hood” with us. There is no obligation to change accountants, but we give you a second opinion if you’re paying too much tax.

Throughout that process, we can identify any problems we see with your current setup. Anything that your current accountant hasn’t claimed, or tax you may have overpaid, and strategies of how we might fix that going forward. We can run through with you once you book with us.

Your Last Chance To Carry Back Business Losses

This is the last year in which, if you have a loss in your company, you can carry that loss and apply it back to any prior years where you’ve made a profit.

There are limitations in how far back you can go, and there’s a process to that. If your company has gone through a loss this year, chat with your accountant and make sure that we get that tax offset. Essentially, you get a rebate on your tax bill for the prior years.

If you’re keen to explore changing accountants, we have a non-obligation process to do that. The first step is booking a strategy call with one of our accounting team. It’s a free 20-minute zoom or phone call where you get to meet us to manage your questions.

From that point, you can consider doing a “Look Under The Hood” with us. There is no obligation to change accountants, but we give you a second opinion if you’re paying too much tax.

Throughout that process, we can identify any problems we see with your current setup. Anything that your current accountant hasn’t claimed, or tax you may have overpaid, and strategies of how we might fix that going forward. We can run through with you once you book with us.

Finding Balance Within the Allocation of Profits within professional firms Guidelines PC 2021/4

The industries that are affected by the Allocation of Professional Firm Profits Guidelines are the service-based businesses where you are selling knowledge or expertise. If you are using a trust or a company to run your service-based business, they want to attribute as much money as they can in the expert’s (owner’s) name.

Let’s say Ben Walker runs Inspire; the more profit that ends up in his personal name, he gets taxed at a higher rate, and the less risk the ATO deems on potentially breaking these guidelines.

The guidelines provide a self-assessment risk framework broken into three zones:

- Green = low risk

- Amber = moderate risk

- Red = high risk

The higher the risk, the more resources the ATO will allocate to understand the existing arrangement and may request you to make the required adjustment. The ATO may proceed with an audit if the arrangements remain high risk.

It doesn’t mean 100% of your business’ profit needs to end up in your own name, but we need to find the balance that we see as fair where we sit within these rules.

If you’re keen to explore changing accountants, we have a non-obligation process to do that. The first step is booking a strategy call with one of our accounting team. It’s a free 20-minute zoom or phone call where you get to meet us to manage your questions.

From that point, you can consider doing a “Look Under The Hood” with us. There is no obligation to change accountants, but we give you a second opinion if you’re paying too much tax.

Throughout that process, we can identify any problems we see with your current setup. Anything that your current accountant hasn’t claimed, or tax you may have overpaid, and strategies of how we might fix that going forward. We can run through with you once you book with us.

Don't Miss Out On These Tax Benefits

For small business owners,

The first thing that everyone’s been thinking of and waiting on is the temporary full expensing rules.

Just a quick reminder, for assets that were purchased in this financial year, this will be the last time where there is no limit on what you can claim as a tax depreciation not withstanding cards.

That was earmarked to end on the 30th of June and there’s no extension of that rule itself.

Where it does fall back on?

We have a temporary one-year increase to the instant asset write-off threshold, which is going to be $20,000. It’s going to be for one year, which is next financial year from 1st of July, 23 to 24. And that’s where any assets purchased below $20,000, you can write that off immediately.

If it’s above $20,000, we fall back to the old ways, in which you depreciate it at 15% for the first year, and then 30% the year after until the value of the asset is below $20,000. And we can write it off straight away.

If you’re keen to explore changing accountants, we have a non-obligation process to do that. The first step is booking a strategy call with one of our accounting team. It’s a free 20-minute zoom or phone call where you get to meet us to manage your questions.

From that point, you can consider doing a “Look Under The Hood” with us. There is no obligation to change accountants, but we give you a second opinion if you’re paying too much tax.

Throughout that process, we can identify any problems we see with your current setup. Anything that your current accountant hasn’t claimed, or tax you may have overpaid, and strategies of how we might fix that going forward. We can run through with you once you book with us.

The New Tax Strategy For EV Buyers

The government is encouraging the uptake of electric vehicles with this new strategy. If you buy an electric vehicle before the end of this financial year (30 June 2023), you can claim it as a tax deduction in your business.

Previously, if your logbook had 50% business use, and 50% private use, you could only claim 50% of the car in your business.

But what’s happening with the electric vehicles, regardless of what that percentage use is, even if it’s 50% personal use and 50% is business use, you can claim 100% of it still. Since it is FBT exempt there are no tax consequences.

It’s beneficial for professional people who don’t travel much and usually have less of that logbook percentage and are able to claim really less of their cars anyway.

NOTE: This would have some impact on your reportable Fringe Benefits on your tax return which can change HECS payments and some other government benefits.

Watch the full webinar, Tax Planning in 2023 and learn the tax saving strategies business owners need to know before 30 June at https://youtu.be/dqE_6X7utjM

If you’re keen to explore changing accountants, we have a non-obligation process to do that. The first step is booking a strategy call with one of our accounting team. It’s a free 20-minute zoom or phone call where you get to meet us to manage your questions.

From that point, you can consider doing a “Look Under The Hood” with us. There is no obligation to change accountants, but we give you a second opinion if you’re paying too much tax.

Throughout that process, we can identify any problems we see with your current setup. Anything that your current accountant hasn’t claimed, or tax you may have overpaid, and strategies of how we might fix that going forward. We can run through with you once you book with us.

Eligibility Criteria For Training Tax Deductions

Claim an additional 20% expenditure

Claim an additional 20% of expenditure that is incurred for the provision of external training courses to their employees.

Eligibility

- Small Business

- Employee is in Australia

- Course is provided by a registered provider in Australia

Make sure that not only does your entity qualify but also that the money you’re spending it on.

Suppose your bookkeeping has been done for this financial year, and you’ve reconciled the training clearly. In that case, you should talk with your accountant to ensure they have been accurately recorded and accounted for.

* This measure will apply to expenditure incurred in the period commencing from 7:30 pm AEDT 29 March 2022 until 30 June 2024. Please note: These measures are not yet law.

If you’re keen to explore changing accountants, we have a non-obligation process to do that. The first step is booking a strategy call with one of our accounting team. It’s a free 20-minute zoom or phone call where you get to meet us to manage your questions.

From that point, you can consider doing a “Look Under The Hood” with us. There is no obligation to change accountants, but we give you a second opinion if you’re paying too much tax.

Throughout that process, we can identify any problems we see with your current setup. Anything that your current accountant hasn’t claimed, or tax you may have overpaid, and strategies of how we might fix that going forward. We can run through with you once you book with us.

Get Cashed Up

©2025 Inspire Accountants - Small Business Accountants Brisbane All Rights Reserved

Liability limited by a Scheme approved under Professional Standards Legislation.