New Years Resolution: 5 Urgent Reasons to Change Accountants in 2015

Most business owners are not happy with their current accountant. So why don’t they change accountants?

Studies show that we sometimes prefer working with the devil we know, to avoid the unknown or the adventure. This avoids the question mark while we find comfort in the norm.

But what if the norm is costing you money?

What if you found an accountant that could provide the insight you need to grow your business?

And do keep in mind that accountants are not all equal. It’s like comparing apples and oranges.

While this article is a bit of a shameless plug, I’ve put together a list of 5 urgent things you must get from your accountant in 2015.

1. Get insight from your numbers

I believe this is the main role an accountant should be providing you as the business owner.

Businesses benefit the most who work with an accountant that is constantly providing insight into their numbers.

Interpreting monthly results, analysing sales trends, planning, forecasting and helping to measure key numbers.

2. Plan your 2015 year

It’s important at the beginning of the year (or preferably before it starts) to plan for your 2015.

You need to review the past, and plan based on what you can achieve in 2015.

We’ve got a live planning workshop coming up in mid-January that will help you with exactly that.

3. Track your key numbers

Tracking your key numbers is a must – and a concept reinforced in the book ‘4 Disciplines of Execution’. You must keep score, and ideally in a visual way too.

For this, it’s best to have a live dashboard – something that both you and your accountant can see as it happens.

There are numbers that are harder to track in a live form, such as ‘number of sales meetings per week’. For this, you can use Jerry Seinfeld’s star method.

4. Adopt cloud accounting

If you haven’t already gone to cloud accounting, the time is now!

This is a no-brainer. The amount of time, effort and dollars that cloud accounting saves businesses is astounding.

Cloud accounting gives many benefits to businesses including:

- Automating menial tasks adding up to hours

- Bank data feeding in automatically

- Integration with other cloud business applications

- Real-time access to accounting data

5. Carry out tax planning

Tax planning is another area where accountants need to lift their game.

A good friend and consultant to the accounting industry says, “Accountants take the term ‘tax agent’ a little too seriously”.

Tax planning needs to be:

- Done immediately if it hasn’t been carried out before – often additions or changes to your business structure is required.

- Performed on an ongoing basis – at least every 12 months (we carry tax planning out annually for our business clients in the May to June period of each financial year).

It’s also important that your tax planning needs grow with the size of your business. When you’re starting out, there’s less scope for tax planning compared to when you’re going flat strap and shooting through the tax brackets.

How do you change accountants?

So the steps to change accountants might be a little daunting, but really the process is simple.

1. Find the right accountant for your business (we put together this list of 10 questions to help you);

2. It’s best you give your previous accountant the heads up with a phone call;

3. Your new accountant writes what is called an ‘ethical clearance letter’ informing of the change and requesting any records they need.

Just to clarify that third step, your new accountant can help with the process of retrieving the right information from your previous accountant.

Oh, and one last shameless plug: give us a call on 1300 852 747 or contact us if you are looking to change accountants who focus on the stuff that matters.

Don’t Break the Chain: How Jerry Seinfeld measured success

A few months ago, I was reading a write up about Jerry Seinfeld and how he tracked and measured success.

The concept that he shared was to track visually, on a calendar, the days that you complete a task.

For each day that you complete the task, put a red star on the day. After a while, you’ll see a chain of red stars and the goal then is to ‘not break the chain’.

![]()

Click here to download the 2015 calendar in PDF.

What could you track using this system?

It all depends on your goals, and you could also implement one at home, and one for work too.

You could track the days that you:

- go to the gym;

- write a ~500 word blog article;

- clear your emails;

- meet with one of your clients, and so on.

Remember to measure what matters to you and your business. I wrote an article earlier in the year on ‘The One Number‘ which goes into a bit more detail on choosing a metric to measure like this.

The visual incentive to ‘not break the chain’ is what spurs you on.

Alternately you could use a similar system if it’s only a few times each week that you need to hit your target. For instance, you probably shouldn’t go to the gym every single day, so you could aim for an average of 5 times per week – and also track this on the calendar.

We’ve put together a template for you to use, for both weekly and monthly goals to track visually.

Also if you’re chasing an editable version of the above calendar to tailor it that fraction more, here’s a link to the editable file.

You’re Killing Conversion: Why you should stop doing Quotes in Xero

Business owners underestimate the power of good quality proposals and a great conversion rate on their business.

A quote is not a proposal

A proposal, in my books, gets to the heart of your business, why you do what you do, and how you can serve your customer. A quote is simply a price for a transaction on your letterhead. It’s one of the first things your buyers experience, and will ultimately be what they base their buying decision on.

And if conversion rate is important to you, then so should powerful proposals.

In this article, I dive a little deeper into numbers than normal, but bear with me. Here’s what we’ll cover:

- How conversion rate impacts sales

- A case study of how increasing conversion rate can double revenue

- A few tools that can help you increase your conversion rate

I wrote this article because too many of our clients are using the ‘draft invoices’ section of Xero for their quotes.

And while this may be a step up from paper or a Word document, I still think with a little effort and an additional bit of software the quality of proposals, and therefore conversion rate should massively increase.

1. How conversion rate impacts sales

Let’s start with a simple formula.

Leads X Conversion rate = New Customers

You need to know all three numbers above, so you can measure the impact of implementing the suggestions below.

Start by working out how many new customers your business has onboarded over the past 12 months.

Then, I find that most business owners have an idea in their head of what their conversion rate is, but let’s go to leads for a moment.

Leads, in the calculation above, is how many customers have come to you, and asked to know more about how you can help them. This includes inbound and outbound marketing (you went to them too, and they agreed to meet).

To confirm your conversion rate, simply divide New Customers by the number of Leads over the past 12 months.

New Customers X Average Spend = New Sales

Here’s the next formula. Now I want to focus on the relationship between new customers and new sales rather than increasing average spend (although here’s how to increase spend: put your prices up!).

This is simply to help you join the dots.

Leads X Conversion Rate X Average Spend = New Sales

And if we remove the middle man, here’s the two formulas above, put together:

2. A case study of how increasing conversion rate can double revenue

Let’s look at a slight increase in conversion rate, all else remaining the same. We’ll look at a fictional web design business, ‘Inspire Web Design’ or ‘IWD’.

IWD met with 180 leads over the past 12 months (just 15 per month), signed up 55 as clients, and they spent on average $8,400 with IWD.

55 clients / 180 leads = 30.55% conversion rate

180 leads X 30.55% conversion X $8,400 average spend = $461,916 in new sales.

Let’s say that IWD focused on increasing their conversion rate through implementing powerful proposals and touching up their sales process. By implementing this, their conversion went from 30.55% to 55%. Still quite low, right?

180 leads X 55% conversion X $8,400 average spend = $831,600 in new sales.

By increasing conversion rate from 30.55% to 55%, the business almost doubled new sales.

3. A few tools to increase your conversion rate

There’s a few things you can do to increase your conversion rate.

Sales Process

The first, and non-negotiable one is to have a documented sales process. I’ve written a lengthy article on implementing a sales process – something that will produce results on its own.

Powerful Proposals

The second is to touch up your proposals. I use the word proposal, because a quote is not a proposal.

There’s some amazing, easy to set up and use, cloud based proposal tools available that let you include video and images to support your proposals. Most have features such as options in your proposal, online acceptance and signing, custom domain & branding, and creating a proposal from a template or previous proposal.

Some great products that we’ve used for us or clients are:

Quote roller (we use this ourselves for our larger, custom projects)

Quotient (great for tradies)

Others available:

You must spend a few hours setting it up, and even better – get a graphic designer on board to tailor a branded, well designed proposal for your potential customers.

All the best with your conversion rate, and do let me know your questions, comments and observations in the comments section below.

Plan for Profit 2015 – Webinar Replay

Here’s the recording of our “Plan for Profit” webinar – where we share how you can use the numbers to increase profitability in 2015.

We put this webinar together in response to a few comments to help business owners and entrepreneurs plan their year ahead.

In this webinar, we share:

- Bill Gates’ interesting holiday habit

- The Power of One Number rather than many

- Three Ways to Grow Your Revenue

- Tools for Planning

- Plan to Profit Workshop

- Reading list for Christmas holidays

[su_youtube url=”http://www.youtube.com/watch?v=Xzeade7sLcM” width=”640″ height=”360″]

4 Step Planning Workflow Sheet

4 Step Planning Workflow Sheet

Here’s a visual flow of the planning process that we use to map out the numbers in businesses.

4-Steps-to-Planning-the Numbers

Plan to Profit 2015 – Holiday Reading List

You might be familiar with Bill Gates’ almost life long habit, to go away on his summer holidays with a suitcase of books to read.

And for our upcoming workshop, Plan to Profit in 2015, I’ve put together a list of books that will help you put together a strategy, plan and implement for your biggest year yet.

These titles will change your thinking, your business and your life.

Prefer to watch this article?

[su_youtube url=”http://www.youtube.com/watch?v=OHGMW5dFPmY” width=”640″ height=”360″]

Books on Strategy and Execution

The One Thing – Gary Keller

This book really helped me with focus and was recommended to me by a client. With the overall message being to focus on just one thing to make everything else easier or unnecessary.

I enjoyed the book to much, and put together an article on ‘the One Number‘, as most businesses need to focus on just one number in order to make everything else easier or unnecessary.

Along with business, Gary also applies it to your life outside of work.

Scaling Up – Verne Harnish

Wow! Verne calls this “The Rockafella Habits 2.0”.

If you’ve read the Rockafella Habits and have implemented what he’s on about in that, this book will touch up on those points – with tools and templates to cement it.

Verne has gone ‘all out’ with his Intellectual Property here – a $10 eBook, that is actually worth its paperback weight in gold.

There’s all sorts of strategy and planning tools, capped off by the ‘One Page Plan’. A must to map out over the Christmas holidays.

The 4 Disciplines of Execution – Sean Covey

I learned so much reading to this book – especially around tracking your plans visually, around your workspace.

Sean also introduces new language such as:

- WIG’s (Wildly Important Goals)

- Whirlwinds (the whirlwind of business causing us to fall off our plans)

- Finish Lines (specific outcomes you must be able to see)

The four disciplines, which you must read more about in the book, are:

- Focus on the Wildly Important

- Act on the Lead Measures

- Keep a Compelling Scoreboard

- Create a Cadence of Accountability

A really great book, especially for the creative and visual people in your organisation to implement.

Books on Customer Service

It is no mistake that I’ve included a few books on customer service for you to read in your planning.

All to often, we can focus on the financial drivers of our business. The danger is in missing the point, or why we’re in business in the first place: our customers.

This is case in point of why we don’t do timesheets in our accounting firm. (But we do measure things like turnaround time on jobs and broadcast our live average reply time to emails.)

Be sure to read these before you start penning your goals for 2015.

From Worst to First – Gordon Bethune

This is a phenomenal story of how CEO of Continental Airlines, Gordon Bethune, managed to turn around the airline giant from ranking at the bottom, to leading the industry.

A true account of focus, and especially on the customer focused numbers.

It’s just unfortunate that after new management took over the reigns from Gordon, they switched back to focusing on ‘making a profit’ and that is why the airline is no longer around…

Keep your business focused on what matters to your customers!

The Ultimate Question 2.0 – Fred Reichheld

This is a book primarily about the ‘Net Promoter Score’. An indication of how likely your customers are to be advocates for your business.

I also love the chapter on ‘Bad Profits’ – how the bigger businesses are willing to lose face and grow their for the purpose of making profits.

There’s tonnes of practical tips on how to implement the ‘NPS’ mentality into your business, but best of all how to act on the results that you get.

Taking the ‘Numb’ out of Numbers – Brisbane Business News

The original article was published by Brisbane Business News and written by Jenna Rathbone on 27 November 2014.ACCOUNTING 101 is enough to drive some business owners mundane mad, but Ben Walker is turning the tables on the traditional model and the result is proving positive with more clients now saying ‘count me in’.

The Inspire CA founder has built an accounting firm that offers business performance coaching with a focus on understanding the numbers and says many of his clients are often in denial when it comes to the financial side of their business.

Now an increasing number of them are gaining an understanding of how the numbers crunch and in doing so, are playing a proactive role in the success of their businesses.

“At the end of the day the performance of a business comes back to numbers and if they are not healthy then the business goes under,” says Walker.

“In this day and age where things like the global financial crisis wipes out a good percentage of small businesses, I think it is so important to understand the numbers and account for things like the unexpected.”

Walker, who was a finalist in the Brisbane Young Entrepreneur of the Year awards, says he aimed to shake up the accounting sector by providing an alternative business environment for clients and has incorporated a thriving café into his accounting firm (Inspire Café).

“I don’t like the old way of doing things and I wanted to create a firm that our clients enjoy coming to,” says Walker.

“We offer a much different environment to your standard boring accountants office so when a client walks in they are like ‘what is this place?’.

Inspire CA was founded in February 2013 with $30,000 in annual equivalent revenue and grew to employee four people in four months and produced ten times in annual equivalent revenue.

The business has also partnered with B1G1: Business for Good and have integrated the ‘habit of giving’ into both the café and accounting firm.

“For each coffee we sell and email we send, one child gets access to clean water in Malawi,” says Walker.

“For each planning session we hold with a client, we provide training for 75 women in India to learn the skills to run micro businesses to provide for their family.

“We have given 82,170 gifts as a result of our clients working with us.”

The Newstead business also offers meeting room and boardroom hire, a gluten free menu and event hire.

[Award] Brisbane Young Entrepreneur of the Year 2014 Finalist

In November 2014, I was excited to be announced as a finalist in the Brisbane Business News “Brisbane Young Entrepreneur of the Year” awards.

Each year, the Brisbane Business News searches from Brisbane’s most ambitious entrepreneurs who are carving out their own unique position in the business community.

This award recognises game changers in the industry, bringing together innovation, stellar success, disrupting their market with grit and determination.

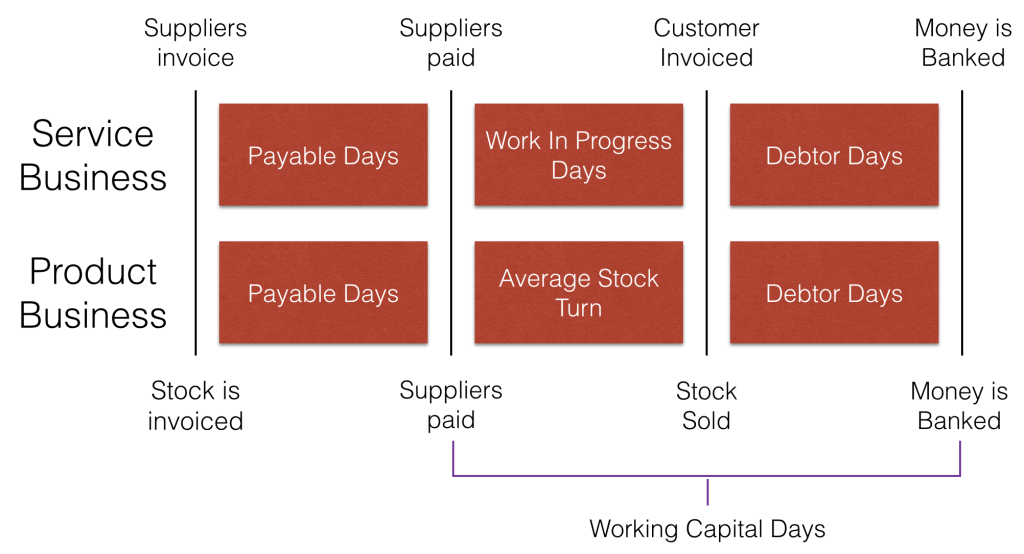

To Increase Cash Flow: Know Your Working Capital Days

We all know that cash is king. And what is more necessary than optimal cash flow in your business?

While Revenue and Profit are a “must” to measure, neither of them give any insight into your business’ cash position. Working capital days gives us the context to Revenue and Profit.

Working capital days is an interesting metric – and it can be broken down into a few components.

In short, working capital days measures the number of days between you paying for your cost of sales, and receiving payment from your customer.

The Goal is to Reduce Working Capital Days

The shorter or smaller the Working Capital Days are, the better the business’ cash flow, as the cash is “tied up” in working capital for the least amount of time.

So if we increase Payable Days, and reduce both Work in Progress Days and Debtor Days, this will reduce working capital days and improve our business’ cash flow.

And yes, it is possible (and desirable) to have negative working capital days!

Calculating Working Capital Days

As working capital is made up of other figures, we’ll need to work out what the following numbers are:

- Payable Days

- Work in Progress Days or Average Stock Days

- Debtor Days

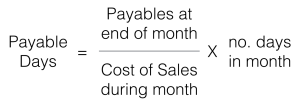

Payable Days

Also called Creditor Days.

Although technically working capital days doesn’t include payable days, the date that you pay your suppliers is the ‘start day’ of working capital days.

So what that means is, if we extend our payment terms with suppliers, we’re shortening our working capital days if all else stays the same.

It’s an important lever to measure, as a few words of negotiating credit terms can reduce some pressure.

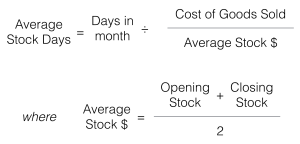

Work in Progress Days or Average Stock Days

Depending on your business, whether service (WIP Days) or selling products (average stock days).

For the service business, I like to refer to WIP days as “turnaround time”. The time from when the job comes in the door, to when it is delivered to the client.

For businesses who carry stock, there is an art to reducing the number of days your stock is sitting on your shelf (and that cash is tied up too!).

For businesses who carry stock, there is an art to reducing the number of days your stock is sitting on your shelf (and that cash is tied up too!).

You can also use this formula as a service business if you put a dollar figure on your WIP.

For those without a dollar figure, please keep a track of your turnaround time using a visual scoreboard or workflow management system. Turnaround time is critical not only for cash flow, but in most cases it matters to your customers.

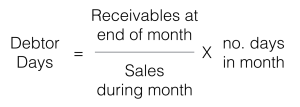

Debtor Days

Debtor days is fairly similar in process to calculating payable days.

Debtor days is calculating using the following formula:

Improve all 3 to Help your Cash Flow

All in all, if you focus on improving all three of the above numbers, then it will have a dramatic effect on your overall cash flow.

Can I claim the kitchen sink? Do’s and Don’ts for Home Office Deductions

With the rise in cloud technology making the need to have a fixed ‘place of business’ outside the home far less important than it once was, many small business owners are choosing to operate from home. Meeting your clients at a decent café is a far more relaxed and friendly environment than a stuffy little serviced office anyway, right?

However, while your business can operate from your private residence with ease, this trend has also created confusion at tax time.

- Which home expenses can you claim as a tax deduction?

- How do you split expenses that are partially private and partially business?

- You used your car for business related trips during the year but are these kilometres deductible?

To help business owners navigate this minefield, we have pulled together the Do’s and Don’ts we usually share with clients who wish to claim deductions for expenses that would usually be seen as private (or ‘non-deductible’ in ‘accountant-speak’):

Household Expenses

The ATO refer to these types of expenses as ‘occupancy expenses’. These include your rent or if you own your house, things like council rates, home and contents insurance and interest on your mortgage. We can also expand this list to include the costs of running the home such as the electricity, water, gas, telephone and internet.

Do claim ‘occupancy expenses’

Before you run off and claim all of your rent in your next tax return, there are some important rules to keep in mind.

Firstly, you need to set up an actual ‘Home Office’. Sitting on the couch with your laptop in front of the TV is not a home office. No questions asked. There needs to be an area in your home set up as a working space specifically allocated to your business.

Don’t claim the kitchen sink (or your floor area that is not an office)

Secondly (and most importantly) you will need to apportion your household expenses based on either the floor area of your home office or the actual usage depending on which expense you want to claim.

To claim occupancy expenses based on the sizes of your home office the calculation is as flows:

(Floor Area of your home office) x $Amount of the expense

(Floor Area of your entire house)

For example, if I have a 200 square metre home and I use a 5 square metre bedroom as my home office, I can claim 2.5% of my rent and other occupancy expenses as a tax deduction in my business’s income tax return.

Do apportion your expenses

Typically some expenses will have a higher business use percentage than that calculated by the floor area method. For example, your home internet and your mobile phone may be closer to 90% business related (if not 100%) so using the floor area method would significantly reduce the available deduction.

In this case you are permitted to calculate a reasonable estimate based on your actual usage. If your usage of your home internet based on hours used is 75% then you can claim that percentage of your monthly internet bill as a deduction.

So which method do you use for each type of home expense? The short answer is whichever method gives you the highest deductible portion, while still being easy to support in the event that the ATO requests evidence.

Do choose which method provides the best deduction

Typically the floor area method will be the most appropriate for occupancy expenses while other home office expenses are usually claimed under the actual usage method.

In the event all of the above just sounds like too much hard work, the ATO does allow a flat rate deduction for home office expenses to cover the extra electricity and deprecation on any furniture used. This deduction is claimed at a rate of $0.34 per hour for every hour spent working from home.

If you are looking to claim your home office expenses on a property you own, its worth keeping in mind the potential Capital Gains Tax (or “CGT”) issues that can arise from using your ‘main residence’ to produce taxable income.

Motor Vehicle expenses

Once you have established your residence as your ‘place of business’, trips from your home to see clients, visit work sites and attend any other business related function are tax deductible.

Do claim your trips from your home office to clients, work sites and engagements

The specifics of claiming motor vehicle expenses for a business owner are the same as those for an employee.

You can claim up to 5,000 work related kilometres per car in a given year without a logbook. This deduction is intended to cover all your motor vehicle expense (fuel, registration, insurance, maintenance, depreciation etc).

Business owners who wish to claim deductions in excess of this amount will need to keep a logbook for a 12 week period, that begins in the financial year you wish to claim the deductions.

The real ‘Do’

The main take away from this article is always make reasonable estimates that you can support when claiming tax deductions. This does not just apply to home office expenses but in all areas of tax.

If you are reasonable with the ATO they’re usually reasonable with you!

Do be reasonable!