$20K instant asset write-off: time to plan your asset purchases

Good news for small businesses, the $20,000 instant asset write-off has been approved by both houses of Parliament and is just awaiting Royal Assent for FY2025-26.

If you’ve been putting off buying that new machinery, tools, or equipment, now is the time to plan. With six months until 30 June 2026, smart planning could deliver significant tax savings.

What’s changed?

The instant asset write-off threshold has been extended for the 2025-26 financial year.

This means eligible small businesses can immediately deduct the full cost of each asset costing less than $20,000, rather than depreciating it over several years.

Who’s eligible?

- Businesses with aggregated annual turnover less than $10 million

- Applies to sole traders, partnerships, companies, and trusts

How It Works

Per asset, not total: You can claim multiple assets the $20,000 limit applies to each individual asset, not your total purchases.

Example: Buy a $12,000 commercial generator, $8,000 computer software, and $6,000 printer in tools = $26,000 immediate deduction in FY26.

Timing matters:

- Asset must be purchased and installed ready for use by 30 June 2026

- Ordered in June but delivered in July? No deduction available in 2026FY

- Purchased in June but not installed? May not qualify

GST exclusive: If you’re registered for GST, the $20,000 threshold is the GST-exclusive price. So a $22,000 including GST item ($20,000 + $2,000 GST) still qualifies.

What Assets Qualify?

Yes: ✓ Machinery and equipment ✓ Office furniture and computers ✓ Tools and work equipment ✓ Commercial kitchen equipment ✓ Retail fit-out items ✓ Technology and software (including purchased software, but not subscriptions) ✓ Manufacturing equipment ✓ Trade vehicles (utes, vans)

No: ✗ capital works, including buildings and structural improvements. ✗ Assets that are leased out, or expected to be leased out, for more than 50% of the time on a depreciating asset lease. ✗ Assets used in your R&D activities. ✗ Software allocated to software development pool.

What about assets over $20,000?

If an asset costs $20,000 or more, it goes into your small business depreciation pool and is depreciated at 15% in the first year, then 30% each year after.

Why early planning matters

- Avoid the June rush-Suppliers get slammed in May/June with businesses scrambling to get assets delivered and installed. Plan now for

- Better prices (unless you can secure a better deal EOFY sale)

- Secure stock and delivery slots

- Ensure installation is completed in time

- Have the asset working for you for longer

- Cash flow management-Spreading purchases across January to June is easier on cash flow than a $50,000 spend in the last week of June.

- Genuine business needs-With time to plan, you’ll make better commercial decisions rather than rushed purchases just to “use up” the deduction.

- Time to explore finance optionsIfyou’re financing equipment, you need time to arrange loans or leases. Starting in June is too late.

Common mistakes to avoid

❌ Buying assets you don’t need – Tax savings don’t justify wasteful spending. A $20,000 deduction saves you $5,000 in tax (at 25% company tax rate) but costs you $20,000 in cash.

❌ Ordering too late – If delivery or installation slips to July, you miss FY26 entirely.

❌ Not keeping invoices and evidence – You need proof of purchase date and when it was ready for use.

❌ Claiming assets not yet in use – Delivered but sitting in a box unopened? Not deductible until it’s installed and ready for use.

❌ Not maintaining logbooks for work vehicles – If you provide an employee (including directors) with a vehicle that they can use for private, it is strongly recommended to maintain a logbook to maximise your tax savings (see above article re: logbooks).

Strategic planning: what to consider now

- Review your asset needs – Ask yourself and check in with employees in regard to: What’s worn out, obsolete, or holding your business back due lack of efficiency? (a simple example could be a slow 4 year old laptop may impact your marketing team ability edit videos fast enough)

- Prioritise and budget – List assets you need, get quotes, plan your cash flow

- Consider timing – Can you stage purchases across the next 6 months?

- Check eligibility – Confirm your aggregated turnover is under $10 million

- Plan for installation – Some assets need professional installation, setup, or testing

- Talk to us – We can help you model the tax impact and optimise timing

Questions to ask yourself:

- Will this asset improve productivity or revenue?

- Would I buy this regardless of the tax deduction?

- Can I afford it without compromising cash flow?

- Is now the right time, or should I wait for newer models/better prices?

What if you’re over the $10M threshold?

Businesses with turnover over $10 million use the standard depreciation rules:

- Most assets depreciate using their effective life (e.g., computers 3 years, car 8 years)

- Still get the same amount of deduction, it’s just spread over longer periods.

Even without instant write-off, planning helps you maximise depreciation claims for FY26.

Why maintaining a logbook is a great idea and an ideal time to start now?

Whether you are claiming work car expenses on your tax return or managing FBT on business vehicles, a logbook could save thousands. January is the perfect time to start one and here is why it matters for both individuals and businesses.

For Individuals & Sole Traders: Two ways to claim

Cents per kilometre method:

- Capped at 5,000 km × 88c = maximum $4,400 claim

- No logbook needed but need to document how you came up with the business KM figure

- Only available to individuals and sole traders

Logbook method:

- Claim business % of ALL actual car costs (fuel, rego, insurance, servicing, depreciation, loan interest)

- Example: 70% business use on $15,000 total costs = $10,500 deduction

- That’s $6,100 more in deductions – potentially $2,000+ tax saved

- Must keep logbook for 12 consecutive weeks (valid 5 years)

Who should use logbook method?

- Driving more than 5,000 business km per year

- High car expenses

- Companies/trusts (cents per km not available)

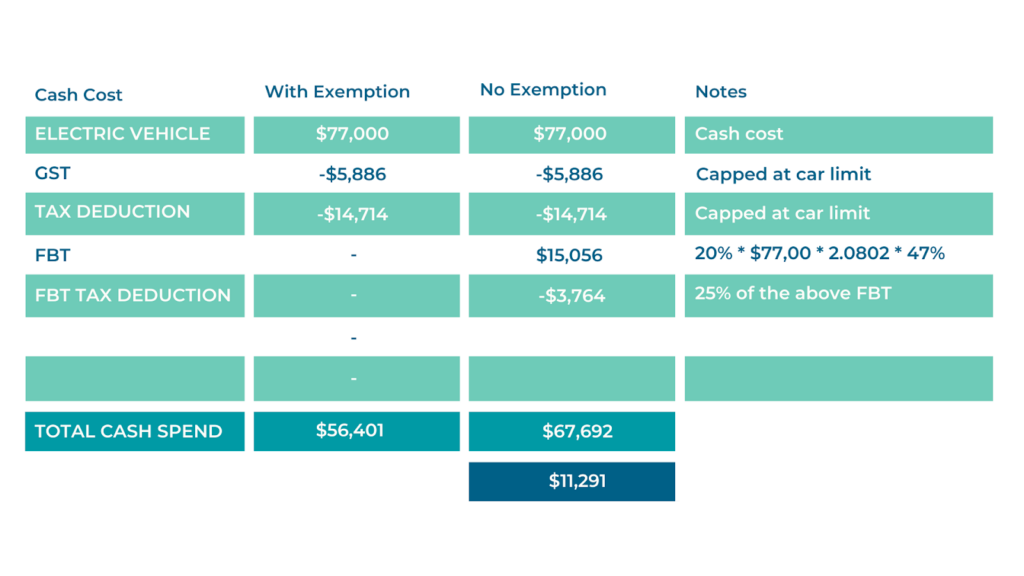

For Businesses: Logbooks may reduce your FBT tax payable or Employee contribution amount

If your business provides cars to employees (including yourself as owner/director), you are paying FBT or making an employee contribution to reduce your FBT. A logbook can significantly reduce this cost.

Two FBT calculation methods:

- Statutory formula method (no logbookrequired)

- FBT based on car’s cost × statutory 20%

- Problem: Even if the car is used 90% for business, you are paying FBT on a high percentage of the car’s value

- Cannot be used for non-car vehicles with private use portion (e.g. Ute with carry load of 1 tonne or more)

- Operating cost method (requires logbook)

- FBT based on actual private use %

- If logbook shows 15% private use, you only pay FBT on 15% of operating costs

- Much lower FBT when business use is high

Example: Company car worth $50,000, total running costs $12,000/year

- Statutory method: FBT on ~$10,000+ (20% × $50,000) = ~$9,400 FBT

- Operating cost method (if 85% business use): FBT on $1,800 (15% × $12,000) = ~$1,700 FBT

- Saving: $7,700 per year with a simple logbook

What you need to record (12 consecutive weeks)

For each journey during the 12-week period:

- Date

- Odometer start and end readings

- Total kilometres

- Purpose (e.g., “Client meeting – ABC Pty Ltd”, “Site visit”)

Plus, odometer readings at start and end of the 12-week period.

Critical: Record ALL trips (business AND private) so you can calculate the business/private split.

Should I maintain a logbook if my vehicle is 100% business use?

Short answer: Yes, you should still maintain one.

Many business owners believe their work vehicle is 100% business use, but the reality is often different when you track it properly. Common “private use” trips that catch people out:

- Stopping at the shops on the way home from a job

- Taking the work vehicle to personal appointments

- Using the vehicle on weekends

- Driving to the gym before work

- Side trips during business travel

Without a logbook, you have no evidence to support a 100% business use claim. If the ATO audits you and finds any private use, your entire claim could be disallowed, or you could face excessive FBT assessments.

For FBT purposes, a valid logbook showing 95% business use is acceptable but claiming 100% business use without any logbook is risky.

FBT-Exempt vehicles: different rules apply

Some vehicles can be FBT-exempt, meaning no FBT applies even if there is some private use. But the rules differ significantly between vehicle types, and many business owners get this wrong.

Commercial vehicles (Utes, vans, trucks):

- Can be FBT-exempt if they are designed to carry loads (one tonne+) or 9+ passengers

- Exemption only applies if private use is minor, infrequent, and irregular

- Examples of acceptable minor private use: driving home after work, occasional detour to drop off supplies

- FBT DOES apply if there’s actual private use like:

- Weekend family trips

- Regular shopping or personal errands

- Taking kids to school

- Using it as the family vehicle

- Important: Having tools or equipment in the vehicle while doing private trips does not make it business use, it is still considered private use

Passenger vehicles (cars, SUVs designed to carry passengers):

- Much harder to get FBT exemption

- Can only be exempt if the vehicle is:

- Parked at your business premises (not at home) overnight, AND

- Not available for private use

- Requires documentation: Written policy restricting private use, annual declarations from employees

- If the car is taken home or available for private use (even if not actually used), the exemption fails

Key takeaway: Just because you drive a Ute does not mean you can use it for personal trips without FBT consequences. The moment private use exceeds “minor and incidental,” FBT applies.

A logbook protects you by showing actual use patterns and providing evidence for your FBT treatment.

Business Travel vs Private: what counts?

Business/deductible: ✓ Client meetings, site visits ✓ Travel between work locations ✓ Business errands (bank, suppliers)

Private/not deductible: ✗ Normal home-to-work commuting ✗ Personal errands, school runs ✗ After-hours personal use

For company cars: Private use includes personal trips by employees/directors AND their family members.

Start in January: here’s why

✓ Finish by March/April, well before EOFY and just in time for FBT year

✓ Valid for 5 years (until 2031)

✓ Captures normal work patterns (not holiday-affected)

✓ Ready for tax planning conversations in April to June

Make it easy: use apps (not sponsored or affiliated)

The following apps can automatically track trips via your phone’s GPS or dedicated tracking devices for more accurate recording:

- Driversnote

- GoFar

Much easier than paper logbooks, though please note these are paid products with subscription fees.

Common Mistakes That Cost You

❌ Recording only business trips (need ALL trips)

❌ No trip purpose recorded

❌ Missing odometer readings at start/end

❌ Keeping for less than 12 weeks

❌ Using expired logbook (5+ years old and pattern changed)

Your January Action Plan

- Record odometer reading now

- Download an app or download logbook template online (many free ones available in Excel/Sheets or PDF format)

- Track ALL trips for 12 weeks

- Keep all car expense receipts

- Send completed logbook to us once completed and we will verify it is compliant and maximise your claim OR minimise your FBT

Private use of Motor Vehicles by Employees and FBT

The ATO has turned its attention to the fringe benefits tax (FBT) implications of employees’ private use of work vehicles.

The ATO believes this is an area that is frequently overlooked by employers.

If your business supplies work vehicles to employees, it’s essential to understand how the vehicles are being used and whether any FBT exemptions apply.

Note: Directors are considered employees for FBT purposes even if they do not receive a wage.

When FBT Applies

FBT generally arises when a work vehicle is made available for private use, even if it is not actually used for private purposes.

Private use includes any travel that is not directly related to the employee’s job, such as:

- Taking the vehicle on beach or camping trips

- School drop-offs and pick-ups (even if on the way to or from work)

- Running personal errands (such as grocery shopping)

- Transporting friends or family for non-work purposes

- Parking the vehicle at the employee’s home, even if this is for security reasons

Important: Carrying tools or work equipment in the vehicle does not change the nature of a personal trip.

If the vehicle is driven for a personal purpose, for example, a weekend outing or a holiday, it is still private use, even if the tools stay in the back.

Exemptions for certain vehicles

Some vehicles, such as specific types of utes, panel vans, or other commercial vehicles, may be exempt from FBT if:

Option 1: FBT law

- Vehicle is not principally designed to carry passengers.

- Private use is minor, infrequent and irregular (e.g. occasional dump run or moving house). “Limited to 2 or 3 occasions in an FBT year”.

- Home-to-work travel is allowed.

- An employer written policy or employee declaration is not required under law (but strongly recommended)

Option 2: ATO Practical Compliance Guideline

PCG 2018/3 gives businesses a clear compliance “safe-harbour” if you meet its rules, the ATO will generally not review your exemption.

To qualify, all the following are required:

- The vehicle is provided for work purposes.

- A written policy is in place setting out the allowable private use.

- The employee signs an annual declaration confirming their use stayed within limits.

- The vehicle is below the luxury car tax threshold.

- The vehicle is not salary-packaged or part of remuneration.

- Private use is limited to:

- Home-to-work travel with minor detours up to 2 km each way; and

- Other private trips totalling no more than 1,000 km per FBT year, with no single return trip over 200 km.

Regular weekend trips or holidays disqualify the exemption, even if the vehicle carries work tools or equipment.

What Counts as a “Written Policy” and “Employee Declaration”?

Under PCG 2018/3, both are essential to demonstrate limited private use.

Written Policy

Your business should have a short document or email that:

- States the vehicle is provided for work purposes only;

- Defines what private use is permitted (e.g. home-to-work travel and small detours only);

- Confirms personal trips must not exceed 1,000 km total or 200 km for any single trip;

- Explains that any other personal use is not allowed (limited to the above); and

- Requires employees to notify you if their use changes.

This policy doesn’t need to be long, one page is enough, but it must exist and be shared with the employee.

Employee Declaration

Each FBT year, the employee should sign a simple statement confirming:

- The vehicle was used mainly for work purposes; and

- Any private use was within the limits set by the policy.

You can use the ATO’s approved declaration template or your own version with the same information.

Keeping these records shows the ATO you’ve actively managed compliance — not just assumed an exemption applies.

If Not Eligible for an Exemption — Valuation of Benefits

Vehicles – Under 1 tonne carrying load (car)

Value the fringe benefit using:

- Statutory Formula Method; or

- Operating Cost Method (you will need a “logbook” to be able to use this method)

Vehicles – Over 1 tonne carrying load (non-car / residual benefit)

Value the fringe benefit using:

- Operating Cost Method (“logbook” method); or

- Cents-per-km Method (if private travel is limited):

- 0 – 2500 cc – 69 cents/km (62 c in 2026)

- Over 2500 cc – 80 cents/km (73 c in 2026)

- Motorcycle – 20 cents/km (18 c in 2026)

Note: If you do not have a logbook for vehicles over 1 tonne and the vehicle is not eligible for an exemption, the private use percentage will default to 100% when using the Operating Cost Method.

This means the entire cost of operating the vehicle becomes taxable for FBT purposes.

Common Issues Identified by the ATO

- Treating private use as business use

- Assuming all dual-cab utes are automatically exempt

- No written policy or declaration when relying on PCG 2018/3

- Poor record-keeping missing logbooks or odometer readings

- Failing to lodge or pay FBT when required

How to Manage the Risk

- Choose your approach: During tax planning discuss with your accountant which option you will be relying on (FBT law or ATO practical guidance).

- Check eligibility: confirm the vehicle design and private-use limits.

- Keep documentation: written policy, annual declarations and odometer readings (if required).

- Maintain a logbook even if you are not required to do so. It’ll give you more valuation options (depending on the car carrying load).

- Ask your accountant to calculate the FBT taxable value using the most appropriate valuation method: Statutory Formula, Operating Cost, or Cents-per-km, whichever yields the lowest tax outcome for your situation.

- Discuss with your accountant whether employee after-tax contributions can be made to reduce or eliminate the taxable value of the benefit and avoid paying FBT altogether. A very common practice.

- If required, lodge your FBT return by the due date and ensure any reportable fringe benefits are included on employee income statements.

⏰⏰⏰ The ugly truth about TIMESHEETS – what old school accountants don’t want you to know about how they charge when they bill you by the hour ??

You may not realise this but ‘Old School’ Accountants charge by the minute.

They are driven by timesheets.

What’s the problem with your accountant charging you using timesheets?

The problem is this…

If the accountant wanted to make more money out of you, what does he need to do?

“Take longer,” you say?

And you would be correct … he could take longer.

But the ugly reality that I’ve seen is this –

“an accountant who does timesheets could either take longer to make more money out of you, or he could just “SAY” he took longer.”

It’s like a dirty Donald Trump locker room secret that most accountants don’t want you to know about – a practice called “TIMESHEET PADDING.”

I’m guilty. I’ve fabricated some pretty spectacular timesheets in my time.

But I was expected to by my employer in order to ‘meet budget’.

That’s why I went out on my own to start INSPIRE CA and why we price our jobs UPFRONT and GUARANTEE that your investment in our fees will pay for themselves many times over in tax saved.

So next time you receive a bill from your Accountant ask him or her if they use timesheets to charge and if instead, they could move you to a fixed price or upfront fee so that you know exactly how much your bill will be.

Got a burning question about using Business Structures to save tax and create a family vault?

Book in, to TEST DRIVE AN ACCOUNTANT – a 15 min rapid fire Q & A session with an Inspirational Accountant.

Are Coffee Meetings Tax Deductible?

Ever wondered if coffee meetings are tax deductible?

Anyone who knows me, knows that I’m a big coffee freak. I have about 3 or 4 cappuccinos every day. My favourite coffee shop is Bellissimo. You’ve got to try it. It’s around the corner from Inspire and there’s also one around one from my house. I get it everywhere.

I was down there meeting with a prospective client the other day. I shouted the coffees, of course. I went to pay for the coffees and the kind girl behind the desk asked me, “Would you like a tax invoice?” It made me think, why would I need a tax invoice? Are coffee meetings tax deductible? So I went back to Inspire and asked the accountants this very question:

“Are coffee meetings tax deductible? What about other meetings that include food, are they tax deductible too?”

Here’s what they told me:

You can claim meals while you’re traveling overnight.

If you’re an employee going off to a conference, and you’re away from your usual home, then you can claim that meal.

There’s guidance from the ATO, but budget for about a hundred dollars per night. That means you might be able to go to the coffee club and grab a Bolognese, but I wouldn’t really be going to Jamie’s Italian and getting a full course meal.

You can claim meals supplies as a working lunch.

Say you got a team, this happens quite regularly during tax time, we’re really busy and we tend to work late. We go out and buy Domino’s. That’s fine because that’s all part of keeping the progress going, with regards to our work. If it’s related to our team being able to continue working, then that’s okay.

You can claim meals supplied from an in-house canteen or café.

I know this really cool engineering business in West End, who have a chef in-house and they supply meals to their team, throughout the day. What a great place to work? These items would be tax deductible and exempt of FBT.

You can claim snacks on the road, while you’re going as a business owner.

As a business owner, you might be out and about, meeting with clients throughout the day. Grabbing a coffee and a muffin, here and there, while you’re doing your day-to-day work is A-okay. Again, you’ve got to be reasonable. The ATO isn’t stupid. If you’re putting through 7-course at a gas station lunches, instead of a coffee here and a muffin, it’s probably not going to go down so well.

So there you have it! The 4 rules, with regards to how to make coffee meetings and meals tax deductible.

To conclude, My advice to you, as a fellow business owner is to:

- Focus on whatever investment you make into your business, whether it’s a coffee meeting here or whether it’s a Facebook ad there.

2. Ask yourself the question, ‘What is the return on investment you’re going to get from that?’ I always try to aim for 5 to 20 times our way. This is the focus point for you as a business owner, if it turns out to be tax deductible as a result, well bonus. If it isn’t, move on. There’s no point in trying to spend an hour trying to make a 20 cent tax savings on an orange mocha Frappuccino that you had on the weekend than risk that concern and anxiety that might come from being audited.

3. And most importantly, focus on the biggest bang for your buck!

Got a burning question about Tax, Your Accountant or Business Structures that can save you even more?

Book in to TEST DRIVE AN ACCOUNTANT – a 15 min rapid fire Q & A session with an Inspirational Accountant.

Where to legally store your excess profits, so the tax man doesn’t take half. (HINT: It’s not in Panama!) ???

Imagine you’ve got an amazing business that is trading through a Trust.

You take out some profit to feed yourself, feed your family, put the kids in school and live comfortably.

But you still have some excess profit left over!

If you take it out, you’ll have to pay up to 49 percent tax.

What do you do?

Now the strategy here is actually to set up a company.

The purpose of this company is to receive a distribution from your business.

It’s a distribution of profits of your business.

So here’s where the tax savings come in …

Individuals pay up to 49 percent tax, but companies when they’re receiving a distribution from a trust, they only pay 30 percent tax.

So paying that profit to a company instead of an individual will save you 19% tax – 49% minus 30%.

Important: You can’t just do this distribution ‘on paper’.

The cash must go from your business into your company and into the company bank account.

Then you can use that money to invest in anything else like commercial property, residential property, you can invest in shares with the money in the company.

You may know these company structures by the following names –

- A company

- A Pty Ltd

- A corporate beneficiary and even

- A Bucket Company

I like to think of it as your “Family Vault”.

It’s a smart place to store the profits your business AND reduce the amount of tax you’re paying.

Got a burning question about using Business Structures to save tax and create a family vault?

Book in, to TEST DRIVE AN ACCOUNTANT – a 15 min rapid fire Q & A session with an Inspirational Accountant.

Pay Less, Little and No Tax in SMSF. It’s legal.

In every Self Managed Super Fund there are 2 sides. An Accumulation side and a Pension side.

Using Harvee’s plane analogy from the beginning, the accumulation side or phase of an SMSF is when the fund is actively growing. The same as when that plane is climbing to new heights. You can’t touch any of that money while it’s in accumulation and that accumulation side has a set tax rate of 15% on what it earns.

So step 1 in controlling taxation is saving tax on contributions.

For example, I contributed $30,000 this year into my Family Super Fund – it’s called the Keshi Super Fund, named after a family dog I used to walk.

If I chose not to dump the $30K into super, I would have paid tax on that $30,000 at my highest marginal tax rate of 49%.

So by putting $30,000 towards my goal of becoming a Self Made Success, I saved $10,200 tax because as I’m in accumulation, I paid at only 15% instead of 49% – my plane is ascending!

Now fast forward 33 years and my wealth plane has been ascending higher and higher, it’s 2049 and I hit what is called preservation age, which means the government allows me to start accessing my super.

The plane begins its descent towards landing at retirement, so I am allowed to bring some of my assets in the SMSF over to the Pension side.

Any idea what the tax rate is on the Pension Side?

Zero percent. Booyah!

So that $30,000 I contributed last year, not only did I save $10,200 on the contribution, but so too did the other 3 members in my Family Super Fund.

With the $120,000 now in the fund, from 4 members contributing $30,000, we used that as a deposit to buy a $500,000 Commercial Property.

If we held on to the property for 34 years, and let’s say it doubled in value over that time and it’s worth $1,000,000.

I can sell the property when the SMSF is in pension phase and pay ZERO tax on that $500,000 capital gain.

WOW, WOW, WOW.

Just to give you some context, If made the exact same property deal but brought it in my own name, outside of super, I would have had to pay $122,500 tax (based on my top marginal tax rate of 49%)

So that’s how the Accumulation side and Pension side of an SMSF work – 15% in accumulation 0% in Pension.

But that’s not all …

What if I told you we could use negative gearing inside of a Super Fund to turn that 15% tax rate in the accumulation phase, down to ZERO?

That is legit possible.

There’s thousands of us SMSF Millionaires who implement this strategy every day.

Week 3 of the Become a SMSF Millionaire, 12 week course the lesson is called “The SMSF Millionaire’s guide to paying Less, Little and even NO tax in your SMSF”. It’s very hard to get ahead if 50c of every dollar you earn is going to the Tax Man.

You can watch the entire Become a SMSF Millionaire Web Class at www.smsfmillionaire.com/go

Accelerated Asset Depreciation – 100% deduction NOW if it’s under 20 k.

How does this strategy work?

You buy an asset.

A car for example.

For running around doing quotes onsite.

Its value will GO DOWN (aka depreciate) over time.

So the tax man lets you claim that depreciating value – Thanks, Tax Man!

The key to THIS strategy is the magic number of $20,000.

If the asset is $20,000 and under you get 100% tax deduction NOW.

Option 1 (Without Tax Planning): Buy a company car for $20,001.

You can claim depreciation … bit by bit over the next 8 years. Sad Face.

(If you want the detail, here’s how much depreciation you could claim in the first year: Only up to a maximum of $5,000 in the first year, but this amount gets lower the further into the financial year that you buy it. If you buy the car on 30 June, you would only get a $13 tax deduction!! boring…)

Option 2 (With Tax Planning): Buy a company car for $20,000.

You get a 100% Tax Deduction this year. Woohoo!

By purchasing an asset $20,000 and under, you’d save $9,400 tax, when compared to paying 47% tax in your own name.

BOOM.

So if you were already shopping for a new asset for the business, remember the magic number – $20,000.

- The Coffee Machine for the Cafe

- The Squat Rack for the Gym

- The Drill for the Sparky

- The Abacus for the Accountant (lol)

- The Scanner for the Doctor

- The Microphone and Laptop for the Podcaster

- The Deep Fryer for the Cook

- The Pole for the Dancer

- The Table for the Physio

- The Camera lense for the Photographer

What do you need to implement this strategy?

- A Business that turns over under two million dollars ($2,000,000)

- An invoice for an asset under $20,000 or under $22,000 if you are GST registered and the expense has GST on it.

- A chat with an Inspire Chartered Accountant – www.calendly.com/inspireca.

- To take action prior to 30 June.

FAQ’s: Accelerated Asset Depreciation.

Why have I never heard about this strategy?

This strategy has been around since May 2015.

Your accountant should have made you aware if they’re a good adviser for your business.

Why $20,000?

This is the limit that the ATO advised in the May 2015 budget.

What if I turn over more than $2,000,000 can I still use the strategy?

No, sorry. The strategy is only available for what the ATO calls ‘Small Businesses’ – those who turn over less than $2,000,000.

NEXT STEPS: You can book in a Quick 10 Min Chat here with an Inspire Chartered Accountant to talk about Tax Saving Strategies that will work for you.