Benefits Of A Self Managed Super Fund

The tax rate of a self-managed super fund is 0% and this is not a trick like the trust was. In certain conditions, your self-managed super fund can actually pay 0% in tax on what it earns. The differentiator between the two is the 15% tax rate is what you pay when you’re accumulating your balance in super. The 0% tax rate is what you pay when you’re taking out a certain type of pension and you meet the requirements to have that concessional tax rate of 0%.

We don’t have any clients running businesses in their self-managed super funds, but we have a number of clients who own businesses in their self-managed super funds. We have clients that are earning significant amounts of money in their self-managed super fund from a business that are paying 0% in tax.

It all comes down to the structure that the actual businesses run out of. There are requirements to owning businesses in self-managed super. It is not as easy as setting one up, there are a lot of things you need to tick off, paperwork you need in place and you need to make sure you are doing what you need to do from a compliance perspective too.

At the start of tax planning, the maximum amount of tax you’re paying in super is 15%, which is almost half a company tax rate or a third of an individual’s highest marginal tax rate, so it’s sensational from a tax planning perspective.

In terms of asset protection, a self-managed super fund is not just a separate legal entity like a company is to a sole trader, but it is protected against bankruptcy. And that’s assuming that you haven’t just known something bad is happening and just chuck a whole heap of money in your super fund thinking it’s safe.

If you’ve made inconsistent contributions to your fund lately, they can most likely be unwound in the case of bankruptcy. But if you’re making $25K contributions a year, for 10 years, and then bankruptcy happens in the last year, they’re not going to say that your $25K is out of character but superannuation balances are normally protected from bankruptcy,

Need to speak to an accountant? Book a ZERO cost 20 minute strategy call with an Inspire Accountant at https://inspire.accountants/chat

The Pty Ltd Business Structure Explained

How you tell someone has a company in their structure, is the letters “Pty Ltd” at the end of the name. For instance, our own structure is Inspire Accountants Pty Ltd. So we’ve got a company within our own structure.

There are two tax rates. The first one is 30% and that was around for years and years but now it has changed over the last handful of years, where 30% is for non-businesses or investment companies (passive investments) The tax rate at the moment for small businesses under the threshold is 26% tax and if you compare it to the highest rate of an individual, it is a lot less.

If you earn $100K in profit in either of these structures, you can easily see that using a company would save 17% or more. It’s a cool way to save a heap of tax just by using that different structure.We call this a small business concession or the small businesses concessional tax rate for the company.

GST can apply in any of these entities and in terms of tax planning for a company, we do get a lot more flexibility. A company like a Pty Ltd company is a separate legal entity, it has separate assets and is considered as separate for legal purposes then the director running the company. So, on a surface level, if your company gets sued, you do have a layer of protection between your personal assets and the company’s assets.

Register to our next event.

Draw Vs. Loan - What's The Difference?

A way to take money out of a company is through a loan and it’s quite complex. If you have a company structure you might have heard your accountant talk about this thing called Division 7A, or maybe a frustration with company loans.

Division 7A basically says you can’t just rip money out of a company with no recourse as a loan. We’ve got to pay that back over time and with a minimum amount of interest and the rate is set by the ATO.

How that looks on a practical level is, if you were to borrow $100,000 from your company and it was an unsecured loan, you have to pay that back within seven years and with interest. Make sure you are meeting the minimum repayments for that loan. It can be quite tricky and we feel it’s a short to medium-term way of taking money out of a company. There are better ways or better strategies we can use to not get ourselves stuck in this Division 7A problem and if you’ve got it, you will know about it.

We also have loans from trusts and we call these ‘Owner Drawings’ – a common bookkeeping term where we literally take the $100,000 out of the trust’s bank account, there’s no Division 7A requirements or anything like that to actually repay that money. It’s great to see trusts are a little bit more flexible when it comes to loans.

Register to our next event.

The Cons Of Being A Sole Trader

What is the highest rate of tax you can pay as an individual or a sole trader in Australia?

The top marginal tax rate is 47%, and it goes higher than that if you’ve got HECS. You can pay north of 50% tax, where literally half of your profit is going to the tax man. If we work our way down to tax planning, we’ve got a list of about 56 tax-saving strategies that we apply every year to see whether our clients are eligible for them and out of those 56, there is only about half of them that we can use as a sole trader. So it’s actually not too flexible from a tax planning perspective, including one of the biggest bang for buck is actually incorporating trusts in your structure.

In asset protection, if you are trading as a sole trader in business and for whatever reason, you get sued as a business owner, then all of the assets held in your personal name are also exposed to that lawsuit so we absolutely do not advocate for business owners trading as sole traders at all.

Need to speak to an accountant? Book a ZERO cost 20 minute strategy call with an Inspire Accountant.

3 Characteristics Of A Trust

Trust is not a legal requirement like the Pty. Ltd. in a company.

The tax rate of a trust is 0% and with a trust, it gives its profit to other people or other entities in the family group and they pay the tax for the trust. However, it is not technically zero because we still need to deal with the profit and get taxed on it from the trust, but we choose who actually receives that profit.

If you don’t choose a beneficiary to receive it, it does actually pay the top rate of 47%. A bit of a technicality, we don’t want that ending up to be the case. But it gives its profit to other people or entities. And asset protection needs to be set up correctly as well.

Need to speak to an accountant? Book a ZERO cost 20 minute strategy call with an Inspire Accountant.

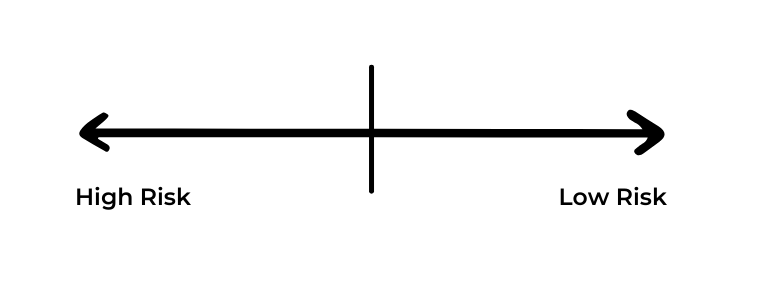

Are You Running A High-Risk Business?

Sole traders are basically the highest risk you’ve got. In terms of asset protection, it is a continuum of how comfortable you are with risk.

What we want to do when clients come on board is educate them on the principles around asset protection and some people start really far around the higher risk side. What we want them to do over the course of working together is kind of slowly move over towards low risk.

In terms of how we might do that, if a company, trust or a combination of the two and its set up correctly, it will take you about halfway along this continuum.

There are still things that can affect it but a company is a separate legal entity and this concept is called the corporate veil. It acts like a wall, so if a missile is shot at your business, there is still a wall that it needs to get through before it starts taking your personal assets.

Need to speak to an accountant? Book a ZERO cost 20 minute strategy call with an Inspire Accountant.

Differences Between Dividends & Distributions

For shareholders who own the company and who are entitled to the profits, you pay a dividend which is a payment of prior year profits to the shareholders. If the dividend is franked, which means the company has paid tax on that amount, the shareholder will receive a franking credit so that they don’t pay tax on the full amount.

If you pay a $100,000 dividend, that would have a 26% or a 30% franking credit, which is the company’s tax rate that it’s already been paid on. The person receiving that money would be assessed on the tax again, less the credit. So they might pay 40% tax that might be their rate, less the 30% credit so they only pay a top-up tax of that 10% difference.

The third way to take money out of a trust is to pay a distribution. The difference between a dividend and a distribution is, a distribution is current year profits. The company earning $100,000, paying $30,000 in tax and paying the dividend out afterwards in the following financial year. If a trust earns $100,000, it has to distribute that money in that financial year. And that’s what we call distributing the current year profits. Otherwise, we get that 47% tax rate that nobody wants.

Need to speak to an accountant? Book a ZERO cost 20-minute strategy call with an Inspire Accountant.

Can A New Business Sponsor A Visa?

We recently invited Michel Sulzbach and Erica Carino, directors of Bravo Migration to a webinar on the topic, ‘Hiring Temporary Residents on a Visa’

Here’s what they said –

Any business could be approved to become a sponsor. The requirements to get a blanket approval are minimal. A sole trader, a partnership, a PTY LTD, a co-op, or any incorporated business that has an ABN, can seek approval to become a business sponsor and once approved, it will be valid for five years.

Government agencies can also sponsor and we had someone in the cabinet who was a sponsor that leaked during the Gillard years, and they were not advocates of this visa. The 485 visa is the descendant of the 457 visa and it was created in 1996 by the Howard government. It is a liberal government creation and a whole skilled migration programme. Labour tends to be vocal against it but when they were in power, there were never that many visas granted under this programme.

In any size and age business, we get a lot of contacts from startups saying, “I really need to sponsor people to get this funding or get this business going, but I’ve heard that startups cannot sponsor.” This is not true. There is no legal requirement that a business must have been trading and operating for a minimum amount of time to be approved. The business needs to be trading, but we have secured approvals even for businesses that technically were not.

One of our large clients is a restaurant and they are very prominent here in Sydney, but now they’re in Brisbane as well. When they started, they needed a chef to be there on the first day when they opened their doors and that chef needed to have work rights on that day, so we had to approve the business even before they opened their doors. We show things like they had rented the premises and they were refurbishing the premises. They had bought equipment and entered into employment contracts. Literally, the day after someone register a business, depending on the case and on the business plan, we could secure an approval for that business.

Watch the full webinar, ‘Hiring Temporary Residents on a Visa’ at https://learning.benwalker.com/courses/hiretempvisas

How To Pull Money Out Of A Company

The first way to pull money out of a company is to pay yourself a salary. It is the context in terms of pulling money out. So, how do you put food on the table through a profit you generate in your company or trust?

There are two things to keep in mind with paying a salary. We’ve moved to single touch payroll over the last couple of years as a requirement for businesses. Once you set your salary, it is kind of locked in and if you want to change it, increase it or decrease it massively. You want this strategy set with your accountant from the start, because of that single touch payroll or what we call as STP.

In terms of salary, the things you have to consider are Pay As You Go tax withholding. There’s a couple of different Pay-As-You-Gos. The W or withholding is the tax that you have to take out of your gross salary which you have to do for your own pay and you’ve got to do that for your team’s pay as well if you’ve got employees and you pay that to the ATO on your BAS. If you take money out through a salary, you have to do the same thing for yourself. And then you also have to pay superannuation on your salary as well.

Need to speak to an accountant? Book a ZERO cost 20 minute strategy call with an Inspire Accountant.

Should You Apply To Multiple Banks For Funding?

We recently invited Scott McGregor, Commercial Broker at Mortar Finance to a webinar on the topic, ‘Funding Your Next Business Acquisition.’

Here’s what he said –

We have conversations with a number of banks to understand their appetites, but generally once we work out each different banks’ appetite, their viewpoint to a transaction, potential structures that they may want to put in place and understand exactly where each bank’s position is, then we have a conversation with our customer to go through those different structures and interest rates, security positions, and all things that are important.

Work out where our preferred option is and then we would apply to that particular bank. Having an application with three or four banks isn’t always the best way to go. It is about understanding which banks can deliver on what sort of criteria, and working at the most appropriate to put an application into. When we apply to a bank they will often do a credit check and the more credit checks you have on your profile within a short range of time can impact your ability to get finance.

It is important for us to understand what our clients are looking to achieve, what banks can help satisfy that requirement and picking the best one but that doesn’t mean bank will come back with an approval, that might mean we have to look at another option, but we do as much research as we can upfront to make sure that when we put in applications on that bank and we figure we have got a better than good chance of getting that loan application approved.

Watch the full webinar, ‘Funding Your Next Business Acquisition’ at https://learning.benwalker.com/courses/fundingbusinessacquisition

Get Cashed Up

©2025 Inspire Accountants - Small Business Accountants Brisbane All Rights Reserved