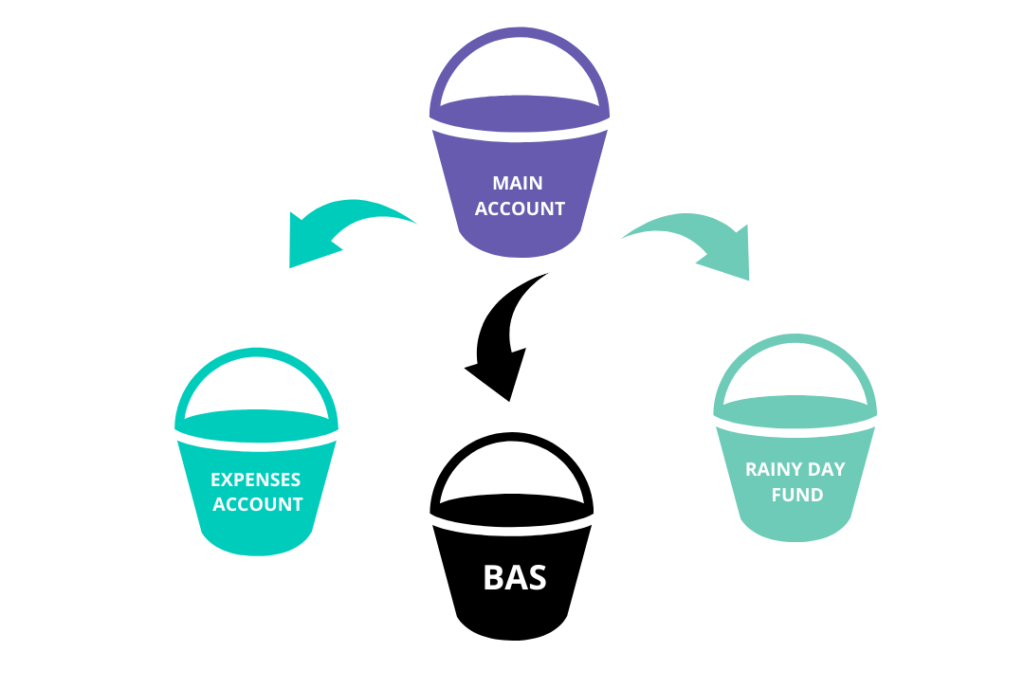

The first one is the main account, it receives all income and it pays the headline expenses which are your pay, the wage bill, and any big suppliers. It disperses the rest into the other accounts.

You want all your income coming into this one, but a handful of transactions going out from the main account. It disperses the rest into these other bank accounts.

Expense accounts pay all the other expenses, the smaller, non-headline or non-critical expenses: things like your Zoom subscription and your email subscription. It can be a credit card that you put this on, but if it will encourage you to spend more money in your business by having it on a credit card and having that limit, don’t do it on a credit card. Just use a bank account and you can always use a credit card later if you are not tempted to spend more because credit cards can be a dangerous thing.

For most businesses, cash flow can be up and down throughout the month. If you’ve got your main account, then you may want to reduce the up and down effect as much as possible and if you’ve got a budget for your expenses, transfer it to your expenses account. If you start running out of money really quickly, you know that you might be spending more than your budget had in mind for that.

Need to speak to an accountant? Book a ZERO cost 20 minute strategy call with an Inspire Accountant at https://inspire.accountants/chat