On a recent webinar, we invited Paul Dunn to talk all things about making your business stand out.

Here’s what he said –

When you become a Standout, people would love to buy from you, you become a magnet for talent, and they would want to work for you. This is a triangle that you should put up on your whiteboard or wherever it is so that you get how important this story is.

And what happens is, when you are that, people look to you because you’re standing out, you stand for, people will respect and recommend you. When more people love to buy from you, then profit and growth would generally be the result.

When people love to work for you because of where you are in your story, They are getting engaged and connected in a way that they’ve not been engaged and connected before, because you’re standing for something more than the dollars that come in the door.

When people respect and recommend you, there will be more profit and growth. So, when you do this, it is good for business.

Watch the full webinar replay, “It’s Not What You Sell, It’s What You Stand For” on our Facebook Page or Book a FREE Strategy Call with an Inspire Accountant.

Are Christmas Gifts FBT?

For tax purposes, a Christmas gift may also be considered as an entertainment.

There are two kinds of gifts:

Entertainment gifts

Items such as movie tickets, concert, airline, theatre tickets may be subject to FBT and not deductible for tax purposes.

Gifts that are more than $300 are subject to FBT. It is likely tax deductible if you are paying an FBT and you can claim the GST. Keep in mind that you will be paying the equivalent of 47% tax on it. If gifts are less than $300, then it’s not subject to FBT and we can’t claim the GST either.

Examples of entertainment:

- Theme park tickets

- Sport/golf

- Leisure activities

- Dinner/drinks

- Movie/concert tickets

- Cruise

- Gift cards for the above things

Non-entertainment gifts

If your business sends chocolate, gift vouchers, pens, or Christmas hampers, this stuff falls outside of the entertainment criteria and you won’t have FBT on it, and it’s most likely tax deductible.

Gifts for employees or clients under $300 are tax deductible without FBT.

Examples of non-entertainment:

- Gift voucher (groceries, health & wellness, books etc)

- Wine or champagne

- Flowers

- Hamper

- Skincare/beauty products

- Perfume

- Computer/TV equipment

Watch the webinar replay, ‘Christmas Parties & Tax – How wine is tax deductible’ at https://www.facebook.com/InspireCA/videos/1544736652557674

What To Watch Out For With Family Funds

In SMSF, it used to have up to 4 members but now it’s gone up to 6 members in the Superfund.

6 people’s balances are better than 1. If you have an average of 100 grand per person and you have 2 people in it, then you’ll have a 200 grand in your fund. And since you got 6, then that would be 600 grand in total. So it’s a lot more money to play with so to speak.

You need to be careful of a few things here:

- Death – What if someone dies and there are 5 members in the fund? How are they going to manage that dead person’s assets and estate when it comes to their superannuation?

- Disability – Are they going to be working together constructively to manage that self-managed super?

- Divorce – If you have two people in the fund like a husband and wife, and they get divorced, they have to act in the best interest of the fund and each other. What if you invited your son or your daughter into your fund and they got divorced but whoever they were with was also in the fund. You need to be very careful when dealing with that situation. You can have up to 6 members but there’s a reason why there’s an average of 2members per fund.

If there are more people, then it equals to more decision-makers or people with their own opinions, and that is another layer of complexity.

You can reduce this risk by a leading member fund and we’ve seen this thing that we can set up called a ‘Leading member fund’ where there is an overall decision maker if people can’t agree. It’s kind of a cool thing to lock in if you want to take better control and you’ve got a few more members than just yourself, and your spouse. And you can convert an existing SMSF to a leading member fund as well so if you’ve already got one, we can change that and set that up to a leading member.

Need to speak to an accountant? Book a ZERO cost 20 minute strategy call with an Inspire Accountant at https://inspire.accountants/chat

In a recent webinar, “Become an SMSF millionaire” we run through the SMSF tax benefits.

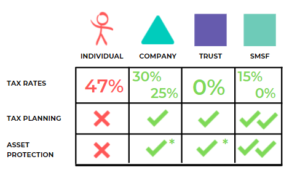

SMSFs have a very low tax environment.

Under trust, it says 0% because trusts like discretionary trusts, give their profit to other entities or people in their family group and they pay the tax. 0% is not quite correct for trust but it actually gives it away.

With an SMSF, an SMSF pays 15% tax or 0% tax on the money it makes. So, they are much lower than the other tax rates and that is kind of a high-level overview of the differences between the tax rates.

Why are there two rates for an SMSF?

The first one is 15% when you’re accumulating your balance over the majority of your lifetime. Then you switch into 0% tax when you’re drawing a pension and when you are over a certain age. You can only get that 0% concessional rate on up to $1.7 million per member in pension. So, if you have $3 million in your own fund balance and in your member balance, then you can’t get that 0% concession on the whole lot.

On the difference. So, on the remaining $1.3 million, if you’ve got the total of $3 million in super, you will still pay the 15%. It’s still low and it’s just not zero. Even if you had $50 million in your own pension account, whatever it earns is taxed at 0%.

Benefits of drawing a pension or being in 0% tax mode plays out if you earn dividends from owning shares in super, then you will pay 0% tax. But some other instances are if you own a business through super, or part of a business, then the profits that go back to the SMSF in that pension account are at 0% tax and similarly if you sell an asset.

So what we see is if you buy a commercial property in your forties or fifties, hold it for 20 years and sell it when you are retired and in pension mode, you can make a massive gain and you can do that without paying any CGT.