The 5 Principles for Asset Protection in Business

Written by Ben Walker, Founder of Inspire – Life Changing Accountants

Written for BSIG – Business Surveyors and Inspectors Group

Asset protection is paramount for building surveyors now more than ever, given the lawsuits that have been seen around Australia. It can also be represented when you have a look at the increasing price of insurance in the industry – what that means is the insurers obviously see higher risk involved for building surveyors.

I want to share five key principles of asset protection for business owners to apply when they’re running their business, structuring the business, and building their own families wealth through the process. It’s important that we don’t go about our lives running a business for 10, 20 or 30 years for something bad to happen in our business and for all that hard work to be taken away.

What I’m not advocating for is being silly about things and being slapdash or not doing a great job – asset protection is a valid strategy and best practice strategy to decrease the risk in the event that something bad does happen.

The five principles of asset protection are:-

1. Separate ‘Risks’ from ‘Assets’

What we want to make sure is that you use a structure such as a company or trust, or a combination of both when we’re looking to structure your business. This company or trust structure should be separate from your personal assets.

We also don’t like to see sole traders or people trading in their own name or a partnership of individuals. A company or trust structure or a combination of both gives you a layer of protection because a company or a company trustee is set up as a separate legal entity from the business owner themselves.

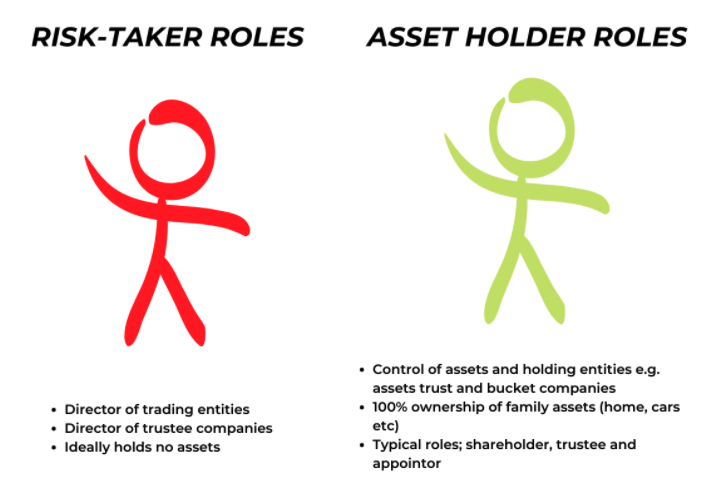

2. Choose a ‘Risk Taker’ and an ‘Asset Holder’ in your family group

If you’ve got a spouse and you’re looking to give your family wealth asset protection, one thing we do with family groups is allocate a “risk taker”, which is usually the key person in the business (or the building surveyor in this context), and an “asset holder” is the other spouse (that’s assuming that our spouse is not in a high risk industry or runs a business themselves).

What we do from that point onwards, is the risk taker is the Director of any trading companies and the asset holders should be in control (but not take on that liability as a Director) – that will be the shareholder or the appointor if it’s a trust structure.

That means that the risk taker should also not own any assets in their own name because what we want is to make sure that they’re an unattractive person to sue if things turn south. For instance, if we’ve got that company structure in place that’s a separate legal entity, there are certain ways that a creditor can get through that; the three main ones are Directors guarantees, fraud, or insolvent trading.

You can look to take the Directors personal assets so the risk taker shouldn’t own much in their own name, if anything, and the asset person should have things like the family home, or be the controller of the family’s wealth. This is quite complex in itself and should always be done with good advice.

3. Separate ‘Business Risk’ from ‘Business Assets’

This is a strategy that I’d say is the next level from a basic business structure of the company or trust. What we do here is, we have an asset holding entity that is specifically set up for business assets, such as; intellectual property, trademarks, patents, logos or designs, business names, equipment, cars, trucks – all that sort of stuff.

What we do with this asset holding entity is license the intellectual property over to the trading entity and so your value of this IP is protected if the trading entity is sued or wound up for whatever reason, you’ve got another layer of protection.

4. Different businesses should be in different entities

If you operate multiple businesses, or even multiple business units, these should operate from different companies, trust, or a combination of that. So what we want to make sure is that if you’ve got multiple businesses or business units, that if one is taken down it doesn’t take all of that with it.

A sign where you might consider setting up separate entities is if you operate in multiple states and have an entity for each state or if you’ve got different licensing requirements between states or even different service lines.

There is a bit of a common sense approach – you wouldn’t want a separate entity with $20,000 of annual income because it’s going to cost extra accounting fees to have another company infrastructure as well. So you want to make sure that it’s worth it and that can be solved by simple conversation with an accountant.

5. Regularly move surplus funds from the risk side of our business structures, to the asset side

How we do that is, we don’t want to make our trading entity end up with a lot of retained earnings or that sort of thing. Any assets that it does have or retained earnings, we want to sweep through dividends or distributions, back to the asset side of our families structures.

That doesn’t mean that the trading entity has no cash but we can do things like loan the trading entity cash from one of your asset holding entities with a secured loan agreement. But basically, what we want to make sure is that the trading entity is a very low desirable thing to sue.

Keep in mind your structures might not be perfect right now.

What we want to do is to shine the light on some of the options that may be available to you in terms of asset protection and the ability to take steps towards de-risking your situation. The other thing to keep in mind is bankruptcy courts can unwind transactions up to four and a half years.

If you were to change your structures now, there is a potential for the courts to unwind those in the case that something bad happened for up to four and a half years. So if you are considering making changes to your existing structure you might want to do it sooner rather than later. As always, please get solid advice from an accountant who knows their way around these asset protection principles because it’s very complex.

Our accounting firm Inspire – Life Changing Accountants, is based in Brisbane, Queensland but we work with clients all around Australia. Given the times we live in at the moment, this is made easy through software like zoom.

We can do asset protection reviews and structure sessions for you and your family based on your existing structures or existing wealth and what your plans are for your business. We can draw this out and share screens with you, so you can follow along if you do need extra help.