Tax Concept – The Right Structure

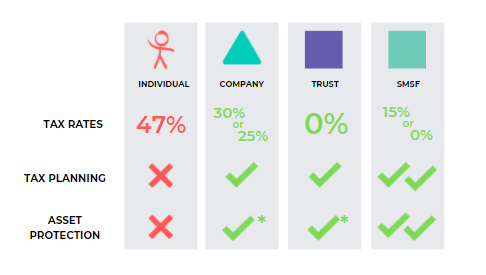

What Tax Rates Each Pays

Individual

One of the big reasons why we might go for trust or company is because of the alarming tax rates where individuals pay up to 47% tax, depending on their income.

Company

Companies have two different rates depending on what the company does. If it’s purely an investment company (so it doesn’t run a business, a business of trading cryptocurrencies, or a business of mining crypto currencies) the 30% tax rate is applicable. The 25% tax rate is for small businesses (so the business of trading, or mining for instance). You need to have most of the company’s income as business income to access this lower 25% tax rate.

Trust

Trust doesn’t necessarily not pay tax, but a trust gives its profits to other individuals, companies, or other entities in the family group, and then they pay the tax on the trust’s behalf.

SMSF

15% tax is what we call the Accumulation phase – where you’re growing your balance in super throughout your lifetime. The 0% is for the pension phase. When you’re drawing on your super, you’re a certain age or older, and you’ve met the conditions of release for super, you will have an option for your super to be taxed at 0%.

Tax Concept – Capital Example

Bob HODLs for 10 years and makes a $1M capital gain.

Bob also works and earns a $120K salary.

Tax just on the crypto profits – depending on structure:

Sole Trader – $230K in tax

Company – $300K in tax (if investment company, and companies don’t have CGT discount)

Extra tax if a company = $70K

So what is the “Normal” Tax Treatment?

WHY WE’RE SHARING

- Ben Walker has personally been an SMSF member since 2011

- He began working with SMSFs in 2007 (before starting Inspire) and his role was heavily geared towards SMSF’s to grow people’s wealth. Since then he worked with hundreds of SMSF’s throughout his career.

- Roughly 28% of our clients have an SMSF, and of those 28%, 60% of Inspires’ SMSF clients hold some sort of property.

- He act as an advisor to many of our clients’ purchases and restructures – so when we get a client looking to buy something, we meet and discuss the best way regarding how to do this.

WHY WE’RE SHARING NOW

- COVID has knocked us all around in some way or another.

- Some businesses still rely on physical premises and still need to meet with clients face to face, for example, medical practitioners and allied health specialists

- There are other businesses that don’t rely on premises, which has dropped the supply of tenants. What we saw early on when COVID arrived is that a lot of people weren’t going to their premises – they didn’t need it when working from home and you’ve got landlords here earning a portion of the rent they used to receive, or nothing at all.

- This is an opportunity for those who need or want their own commercial property to purchase in a buyers market

- Or others who want to buy now before prices get back to “normal”.

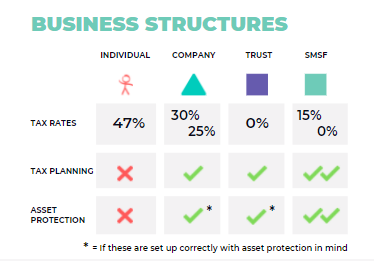

The first thing you have to nail is your business structure. Here’s a quick overview:

Sole Trader – If you’re an individual, you may have to pay up to 47% in tax – meaning almost half of your earnings could go to the ATO.

Company – There are two different tax rates for a Company – you pay a flat tax rate of 25% or 30% (depending on how big your business is). More often than not, it’s 25%, unless you have a passive investment, then it falls in the 30% bracket.

Trust – You don’t technically pay tax in a trust. A trust is like a funnel: it doesn’t pay tax on its own. What it does is it distributes funds to the beneficiaries, which could be a sole trader or company, so you end up paying either 47% of tax, or 25% to 30%.

Self Managed Super Fund – The tax rate for SMSF is 15% or zero. The sole purpose an SMSF is established for is for retirement, so if you have investments in super and you make money there, before you retire you pay 15% on all the income in that SMSF, and once you retire it’s tax free.

Tax Concessions

One of the major concessions that we have is a 50% CGT discount: Say you sell a property and you make $100,000 capital gain – If you held that for more than 12 months you get a 50% capital gains discount. You are eligible for this if you’re trading as an individual, trust, or SMSF (although a 33% CGT discount in super), however, you don’t get this discount as a company.

What We Use

Typically we don’t recommend using individuals or companies as a structure. We prefer trusts and SMSF’s as thats where we drive more of the buying of your commercial properties – the reason why is because of the flexibility that we have in terms of tax planning in the long term, for an unknown amount of gain at purchase.

With a trust and SMSF, you can also effectively plan your asset protection strategies as well as within your family. An SMSF is fairly protected – that’s one of the big benefits to keep in mind if you ever go bankrupt. Yes, you can own your commercial property outside of super, but it is at a higher risk compared with an SMSF.

If you compare all structures, the SMSF structure has one of the best tax environments and you still get your capital gains discount. If you retire and have all these properties or shares that you’ve invested in your SMSF, then you can start selling them, you don’t need to worry about losing a huge chunk to the tax man.

LENDING OPTIONS

OUTSIDE SUPER VS. INSIDE SUPER

Lending Options Outside Super

- Slightly Less Complex Lending

Lending options outside super (so in your own name, company, trust) are slightly less complex lending. - Higher Tax Outcomes

There are also higher tax rates outside of super which is a con doing it outside of super. - Business/Personal Income To Service

There is also business or personal income to service and you can adjust for existing rent if you will owner occupy. - Can Use Other Security For Deposits

You can also use other security for deposit which is unique about lending options outside super.

Lending Options Inside Super

LRBA

For Lending options Inside Super, there is “LRBA” which is an acronym for Limited Recourse Borrowing Arrangement.

Superfunds on their own can’t really lend money from a bank as they’re not supposed to lend in their own right. There are rules where in the right conditions with the right trust set up and loan agreements and if you meet the requirements of the superannuation act, then you can actually borrow using funds with your super and receive the income in your superfund.

Super Contributions And Rental Income To Service

Estimated rental income of the property you’re purchasing along with your super contributions can be used to service the purchase of a property in your super fund. Of course tax is a better outcome on this too – either 15% or 0% depending if you’re in accumulation or pension.

Very Few Lenders (Still Good)

There are very few lenders; 2 main ones but others will consider. The form to apply for a limited recourse borrowing arrangement is less than the one to buy a home. It is however covered by different legislation, so you don’t get the consumer protection.

Typically A Higher Rate

It’s typically a higher rate for lending. Also depends how much of a loan you get as a percentage of the value of your property. If you’ve got a higher deposit on the property, you’re going to pay less on the interest rate.

Needs A Cash Deposit

You cant borrow equity from another property even if it’s another property owned in your super fund. You cannot cross collateralise or access the equity.

Cannot Borrow For Construction Costs Unless Off The Plan

For SMSF lending you can only have 1 loan for 1 asset. i.e. You can’t borrow money for the land and then separately for construction. You can borrow for the land and pay cash for the construction. Or you can buy it off the plan; so 1 contract from a developer where you pay for the land and construction in 1 contract.

Lending Options For Both (Inspire & Outside Super)

Both lending outside and inside can owner occupy for commercial property only. You cannot owner occupy residential. You can see LVR’s go to 80% both inside and outside super. (Sometimes more than 80% outside super given your industry)

Deposit Required

Deposit required depends on the lender, the postcode you are buying in, the asset type (is it an office, a warehouse, standalone free hold or part of a strata title) and the price. The higher the price, the higher the risk to the bank so they might loan you less as a % of the price.

20 – 30% + Stamp Duty

As a guide, stick to 30% + stamp duty and be surprised if they will loan you 80% value. (of course it’s just as a guide)

SMSF’s sometimes need 10% of value of property in liquid cash for lender to be comfortable once settlement has gone through.

For example you may require 30% deposit + stamp duty + and additional 10% in cash in the bank after settlement.

Buying Process

Step 1. Pre-approval

If it’s inside Super, you don’t necessarily need your SMSF set up, so you could be looking but not have an SMSF.

Step 2. After pre-approval and you want to go ahead

Set up an SMSF and bare trust. The bare trust is the lending vehicle. The lead time is 1 to 2 months to be safe for an SMSF setup and what you want to make sure is that when you’re looking to buy something, you need your structure set up to be able to sign the contract in the right name.

OR

You can set up a trust which is a shorter lead time as no there are no super roll overs or third parties to deal with in the setup. Then you can fund the deposit and make an offer subject to finance.

Finally, apply for finance with the contract and if it’s accepted, go through to settlement.

Note – we’re not mortgage brokers, this information was provided by one.

SMSF

INS & OUTS

SMSF cannot borrow to buy property directly

Bare Trust sits in the middle as a “shadow’ purchasing entity

- Lender can be a bank

- Lender can be your own cash (i.e your bucket company lends to SMSF)

The bare trust sitting in the middle is like a shadow purchasing entity. You can borrow from a bank, but you can also borrow from an entity that you control as well. If you have spare cash in a bucket company doing nothing, you could lend that using the right paperwork to your own SMSF, and then to purchase a property. The loan needs to be at commercial terms with interest charged at market value to make sure we don’t breach any superannuation rules.

Buying Outright (No Loan)

It is really simple to buy a property outright with cash and you don’t need an LRBA or bare trust.

Buying Outright (No Loan) Inside and Outside of Super (i.e., $200K Super; $1o0K Personal Funds)

There is a structure that we use, a certain type of trust we can set up where there can’t be any loans on the property, but you can use some money from super and some money from outside super.

Buying In A ‘Suit’ With 2 or more Business Partners (Can Borrow)

You need two or more business partners and this is a different type of trust we use as well, and this one can borrow money from banks etc.

OUR PRICES

Set up $3K + GST

Ongoing from $250+GST/month (3000+GST/year)

- BAS

- Admin

- ESA – Electronic Service Address, It’s a requirement of SMSF where your payroll will send information to our SMSF software to connect it all up with the ATO

- Financials

- Tax Return

- Online Portal

- SMSF Support

Other things to consider

- $350+GST Annual Audit (3rd Party)

- $3-5K Optional advice to advise on set-up

- $3K+GST Bare Trust lending entity set-up

CASE STUDY

Vet from the Bush

We had a Vet from the bush who came to us and said, “Hey, I’ve got a property that I hold outside of super, it’s about $300,000.” He also had a loan outstanding of about $150,000 – which is still a pretty good loan balance at 50% of the loan value of the property.

He said, “I just want to get rid of the bank loan. I know I have enough wealth inside and outside of super to do this, how can I re-strategise the way I hold this commercial property?” Now, this commercial property that he owns, he rents it out to his vet practice. We moved the property that was held outside of super into a Self Managed Super Fund which he paid stamp duty on the transfer. Now, he had enough money to pay out that loan within super ($150k in cash from super). He paid out the loan and the stamp duty and as he also had enough money outside of super, he leant the remaining money to his SMSF as vendor finance.

Here’s the break down:

Step 1. First we moved the property that was held outside of super into a Self Managed Super Fund.

Step 2. There was a loan outstanding on the property personally, which he paid off with cash from the SMSF.

Step 3. How he got the extra funds into his SMSF was to lend from his personal self to the SMSF as vendor finance.

What that means is that he owned the property in his SMSF but the SMSF also owed around $150k to himself outside of super. Now, that’s an important bit to understand and is key to the strategy. What he was able to do was, as his vet practice paid rental income on that property (and as he made super contributions into the self managed super fund) he could repay himself back the money that was borrowed to purchase that property.

This is key because ordinarily when you put money into super, you can’t touch it until you retire. The benefit of doing this transaction was that he was able to clear his loan but also get some money back out to himself over time.

Double your Super Fund

A client’s commercial property owned outside of super was valued at $1,000,000. The client was moving into retirement and wanted to move cash and assets into super.

He did an LRBA loan with a bank, so he moved this property into his SMSF at $1,000,000 purchase price with a $300,000 deposit from super.

As he wasn’t an owner-occupier, it was purely a commercial investment property. For the next three years, the rental income received by the super fund was completely tax-free because he met the retirement conditions. After the 3rd year, he received an offer to buy the property for $1,300,000. And as he was retired and was on a 0% tax rate, he paid no tax on that $300,000 gain effectively doubling his super balance.

Keep in mind that if he bought this commercial property at $500,000 outside of super and it was worth a $1,000,000 when he transferred it in. He’s actually required to pay CGT and stamp duty on the transfer. Due to these transactional costs, we’d need to weigh up the pros and cons in each situation.

In this instance, he made an approximate gain of $300,000 tax-free. All of these case studies are anonymous and have rounded figures for obvious privacy reasons. All in all, that was a fantastic outcome for this client and his super fund was doubled in about 3 years.

IT Business in Melbourne

A client’s business was previously renting and grew through covid.

The business owner had a good opportunity to buy commercial property near home at a purchase price of around $300,000 with their SMSF. The property needed fit-outs such as partition walls and a few other bits and pieces, which were funded through 12 months of prepaid rent by the business as his super fund wasn’t flush with cash for this extra expense.

The fittings and furniture were paid by the business to access the instant asset write-off. The client was essentially paying the same amount of rent but to his own SMSF. More importantly, the capital growth made on the property could be tax-free if sold during retirement.

Home Office to Premises

A client who operates a service business in the building industry has grown through covid. Their existing home office is hitting its limit and has begun to be a bit uncomfortable with a baby on the way.

The client purchased an $800,000 property at around 75% LVR. It required renovations which were funded by their Super fund with cash and the furniture was paid for by the business with instant asset write-offs. As a result, the client now has a lovely shopfront to take him into the next stage of his business’ growth.

Four Business Partners Buying A Property

Four business partners were looking to buy an office space and all of them have self-managed super funds. What they chose to do is purchase the commercial property together equally in their SMSF. They each took $200,000 to pay as a deposit to purchase a $750,000 property plus costs.

This was done through what we refer to as an ungeared unit trust and the purchase was fully cash funded.

Each of the business partners own 25% of the property through their share of the unit trust, thus the self-managed super funds don’t own it directly.

The unit trust essentially owns it outright, so the benefit of that is every time their rent comes through, it gets split 25% each way and if they sell that property, any capital gain made is then split up each way as well.

Watch the full webinar, ‘How to buy your office, warehouse or clinic using your super fund’ on our Facebook Page